This week’s market was a case study in resilience: U.S. equities powered to fresh records despite political gridlock, delayed economic data, and a sharp pullback in energy prices. Investors leaned heavily on rate-cut expectations, inflows into risk assets, and selective sector leadership to keep momentum alive. The S&P 500 and Dow Jones Industrial Average both closed the week at all-time highs, while the Nasdaq lagged slightly on Friday as mega-cap technology names gave back some ground.

Index Performance: Records with Caveats

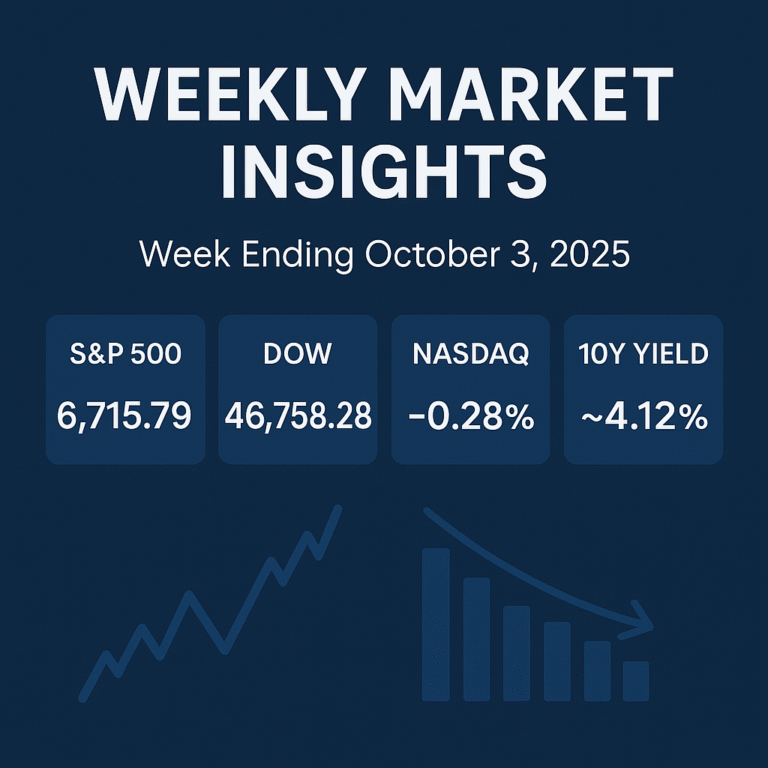

The S&P 500 finished the week at 6,715.79, while the Dow Jones closed at 46,758.28, both notching record closes during the week. The Nasdaq Composite, by contrast, ended at 22,780.51, slipping about 0.3% on Friday as semiconductor and electric vehicle names like Applied Materials and Tesla weighed on sentiment.

Market breadth was a mixed bag. Leadership tilted toward Western Digital, Bio-Techne, Coinbase, Charles River, and Fair Isaac Corp (FICO)—companies that represent storage hardware, biotech research, crypto platforms, and software analytics. These pockets of strength reinforced the idea that while headline indices are strong, leadership remains narrow.

Macro Backdrop: Missing Data, Rising Expectations

Normally, the first Friday of October is dominated by the nonfarm payrolls report. But this week, the U.S. government shutdown—now in its third day—meant that the Bureau of Labor Statistics did not release jobs data. This data vacuum ironically worked in the market’s favor: without hard evidence of labor strength, the narrative shifted to dovish policy expectations.

Several Wall Street banks, including Bank of America, revised their rate-cut calls forward, with consensus building for an October cut by the Federal Reserve, followed by another in December. The bond market reflected that conviction: the 10-year Treasury yield fell to around 4.12%, easing financial conditions and supporting equities with duration sensitivity.

The absence of government data may persist if the shutdown continues, which could leave markets leaning more heavily on Fed communications and private-sector data releases in the coming weeks.

Flows & Sentiment: Risk Appetite on Display

Despite political noise, the inflow picture turned highly supportive. Global equity funds recorded $49.2 billion in inflows in the week ended October 1, the highest in 11 months, with U.S. equity funds and sector ETFs leading the charge. Technology and financials drew the largest allocations, while energy saw modest outflows as crude sold off.

Sentiment surveys confirmed the shift. The AAII weekly sentiment poll showed 42.9% bullish, well above the long-term average, suggesting optimism is climbing even as official data remains frozen. While not at euphoric levels, this confidence highlights a market narrative increasingly driven by expectations of monetary easing rather than incoming data.

Commodities & FX: Oil Retreats, Dollar Firms

The standout move in commodities was the sharp reversal in energy. Brent crude dropped 8.1% on the week, while WTI crude slid 7.5%, marking one of the steepest weekly declines in months. This was driven by a mix of seasonal refinery dynamics and easing supply concerns, a welcome development for equity investors hoping for lower headline inflation in coming months.

The U.S. dollar firmed modestly against peers, reflecting safe-haven flows around the shutdown and positioning ahead of mid-month inflation data.

Sector Rotation: Defensive Nibbles, Cyclical Pulse

Sector rotation was choppy. On Friday, Utilities outperformed while Technology slipped, a defensive tilt consistent with government shutdown headlines. Over the week, however, Industrials, Materials, and select Technology groups still led performance, echoing a cyclical risk-on pulse tied to falling bond yields.

Defensive sectors like Staples and Health Care also saw renewed interest, consistent with the historical playbook during U.S. shutdowns. These are often favored as hedges when visibility is reduced.

Thematic Watch: ARK and Crypto Beta

Cathie Wood’s ARK Invest remained active. The funds added over 500,000 shares of DraftKings (DKNG) this week, a sign of confidence in consumer discretionary growth and digital platforms. ARK also built positions in China AI leaders like Baidu and Alibaba, reflecting their contrarian stance on innovation-driven names even amid geopolitical uncertainty.

Meanwhile, Bitcoin crossed above $120,000 again, lifting crypto-exposed equities like Coinbase. This volatility in crypto markets continues to bleed into growth/innovation ETFs, adding another layer of optionality for traders.

What’s Next: Key Catalysts

Looking ahead, the next two weeks will be crucial.

- CPI Report (Sep) — Oct 15: The first inflation print of Q4 will either confirm or challenge the case for an October rate cut.

- FOMC Minutes — Oct 8: Investors will parse whether the dovish tilt is shared broadly across the Fed or limited to a few members.

- Earnings Season Kickoff: Delta Air Lines (Oct 9) and JPMorgan Chase (Oct 14) headline the opening act. Bank commentary will carry outsized weight as substitutes for absent macro data.

Strategy Playbook

- Rate-sensitive sectors such as homebuilders, utilities, and high-quality growth should continue to benefit if the 10-year yield stabilizes near 4.1%.

- Energy reset opportunities may emerge after this week’s sharp oil drop, but investors should favor companies with strong free cash flow and low leverage.

- Innovation and crypto-linked equities remain attractive but volatile—position sizing and discipline are key.

- Recession-proof allocations in Utilities, Staples, and Health Care remain advisable while uncertainty over government functions lingers.

Final Word

This week underscored the market’s remarkable ability to climb a wall of worry. With indices at records, a dovish Fed narrative, and liquidity flowing into equities, the near-term setup looks constructive. But the combination of missing data, sector concentration, and volatility in commodities and crypto means the path forward will remain uneven.

For traders and investors alike, this is a market rewarding tactical positioning, selective sector bets, and disciplined risk management.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investing involves risk, including the potential loss of principal. No positions are disclosed or recommended in this analysis.