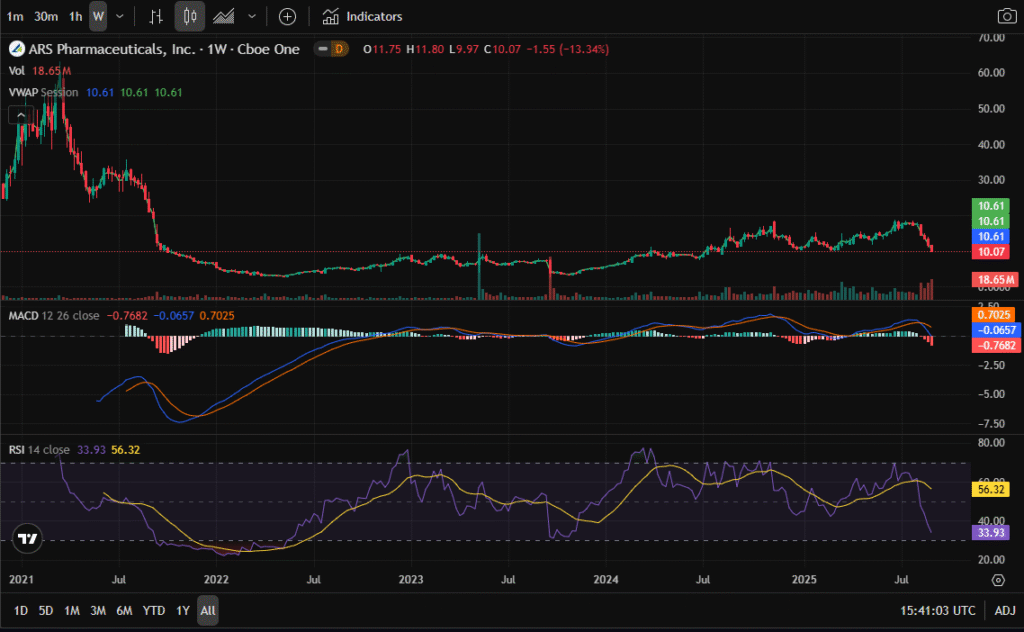

📉 Technical Chart Analysis

SPRY (ARS Pharmaceuticals) recently hit a 1-year low around $10.07, placing it right at the edge of the 52-week range ($9.97–$18.90). On the daily chart, the RSI sits at 20, marking an extremely oversold condition. Historically, SPRY has rebounded when RSI dipped below 30, though oversold conditions can persist in bearish phases.

Meanwhile, the MACD shows a bearish crossover on both 1 year and all time timeframes. The histogram continues to deepen, confirming that downside momentum remains in play. This means that although the RSI suggests a relief rally may be near, the MACD warns that the dominant trend is still lower.

Adding to the bearish setup, volume has spiked on recent down days, suggesting institutional or large-holder distribution. However, this capitulation could also set up the groundwork for a short-term bounce if the $9.50–$10 support zone holds.

💰 Financial Health

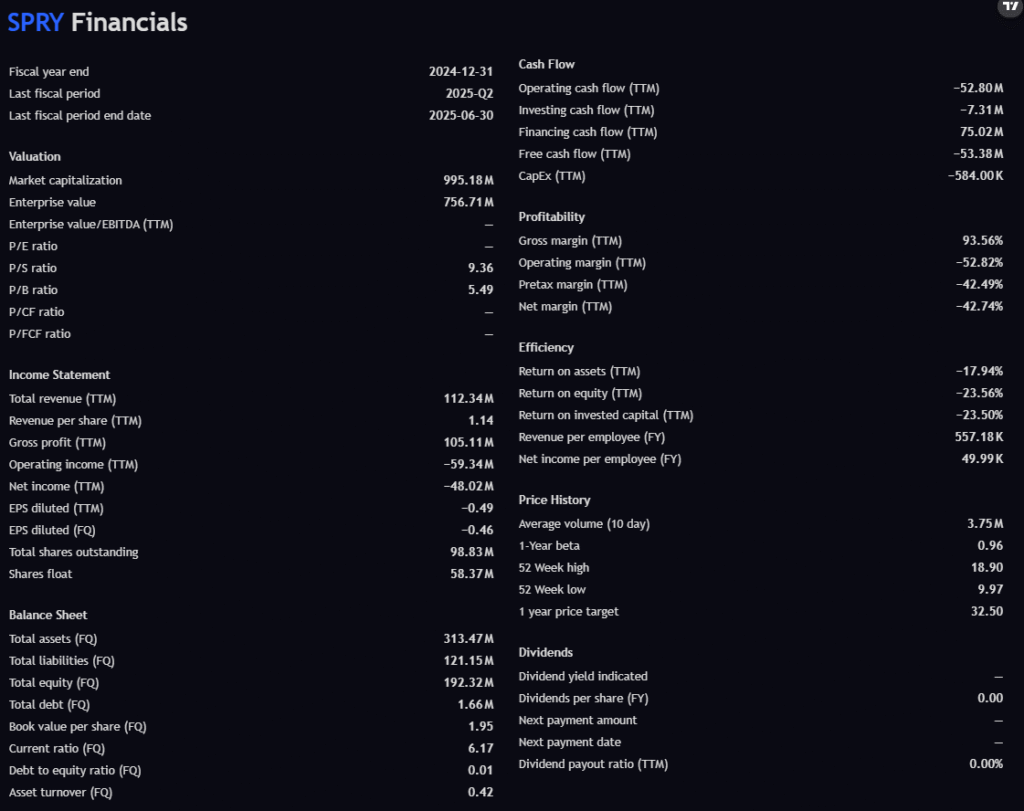

From a fundamentals standpoint, SPRY is a classic early-stage biotech story:

- Revenue (TTM): $112.34M

- Gross Margin: A stellar 93.6% → proves that unit economics are excellent once scale is reached.

- Operating Income (TTM): –$59.3M

- Net Income (TTM): –$48M → consistent losses as the company invests in R&D and commercialization.

- Free Cash Flow (TTM): –$53.3M → confirms cash burn.

- Debt-to-Equity: Only 0.01 → essentially no leverage.

- Current Ratio: 6.17 → strong liquidity runway.

The balance sheet is a major strength: SPRY is not debt-laden and has cash resources to fund operations. However, the high P/S ratio of 9.36 and P/B ratio of 5.49 show that the stock trades on expectations of future approvals, not present profitability.

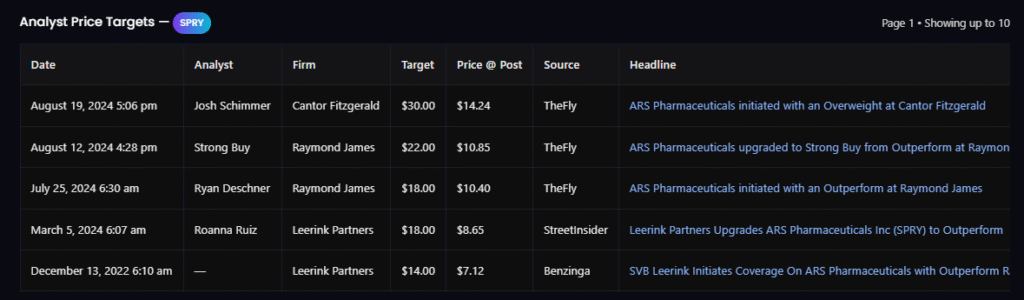

📊 Analyst Targets

Analysts remain very bullish on SPRY despite its sharp decline.

- Cantor Fitzgerald: $30 target (Aug 2024)

- Raymond James: $22 and $18 targets

- Leerink Partners: $18 target

With the current price near $10, even the lowest recent target of $18 suggests ~80% upside, while the high end ($30) implies a potential triple. Analysts appear to be betting on pipeline success and FDA milestones.

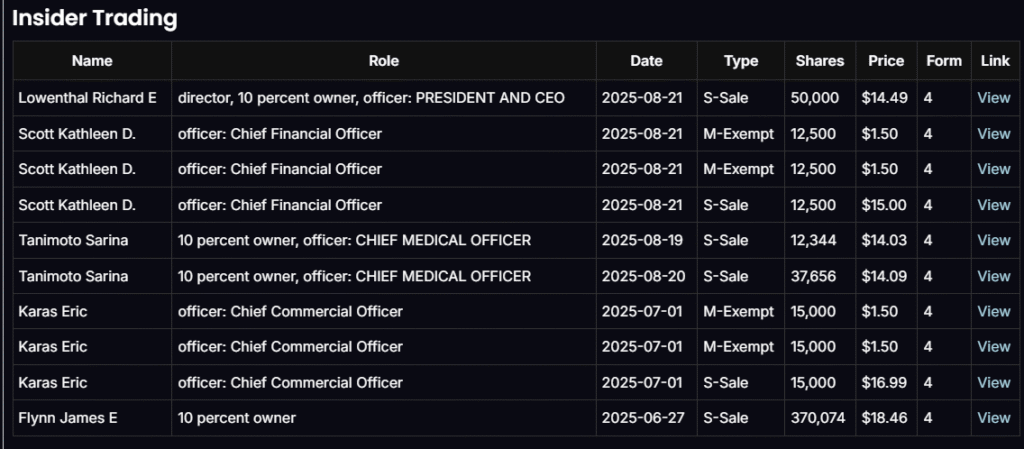

🧑💼 Insider Trading Sentiment

Insider activity, however, has leaned bearish. Key executives including the CEO, CFO, and CMO sold shares between $14–$18 earlier this year, with a large holder unloading nearly 370,000 shares at $18.46.

There has been no insider buying at the current depressed $10 level, which tempers enthusiasm. Insider sales are often timed for liquidity, but widespread selling across leadership raises caution.

🔀 Options Flow Analysis

The SPRY options market shows neutral-to-hedged flows in the near term, but more bullish accumulation further out:

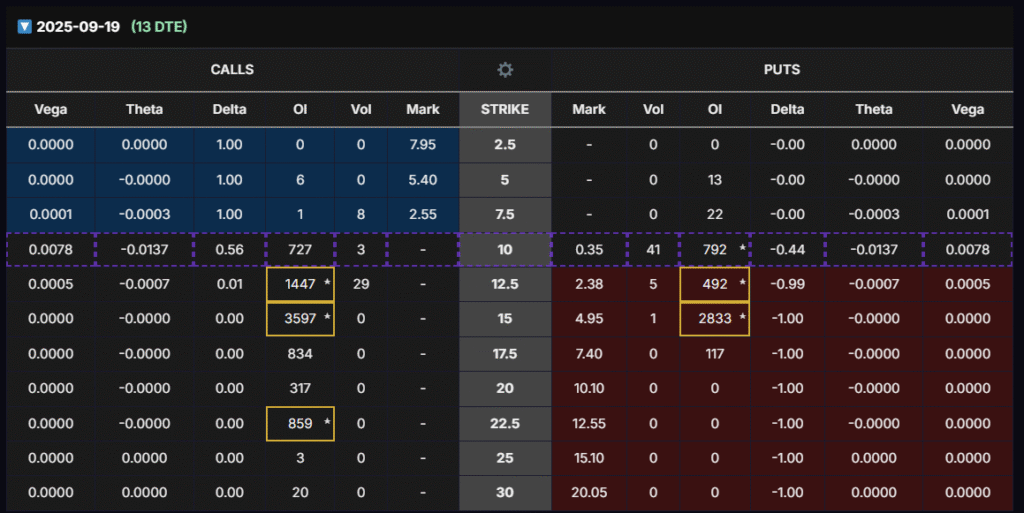

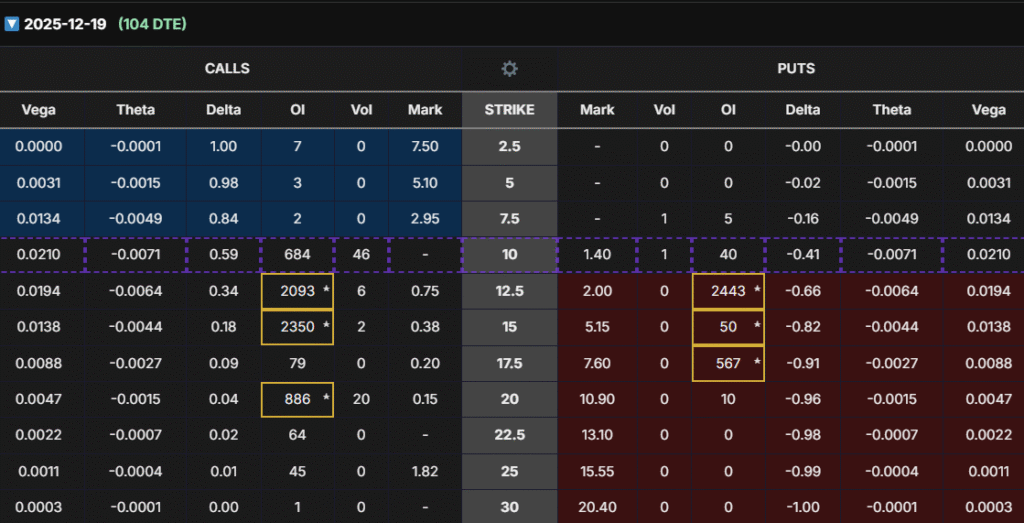

- Sept & Dec 2025 expirations: Open interest is concentrated at both $12.5–$15 calls and $12.5–$15 puts, reflecting hedged strategies (likely straddles/strangles) around volatility events. This positioning suggests traders are bracing for movement but not yet committed to a directional bet.

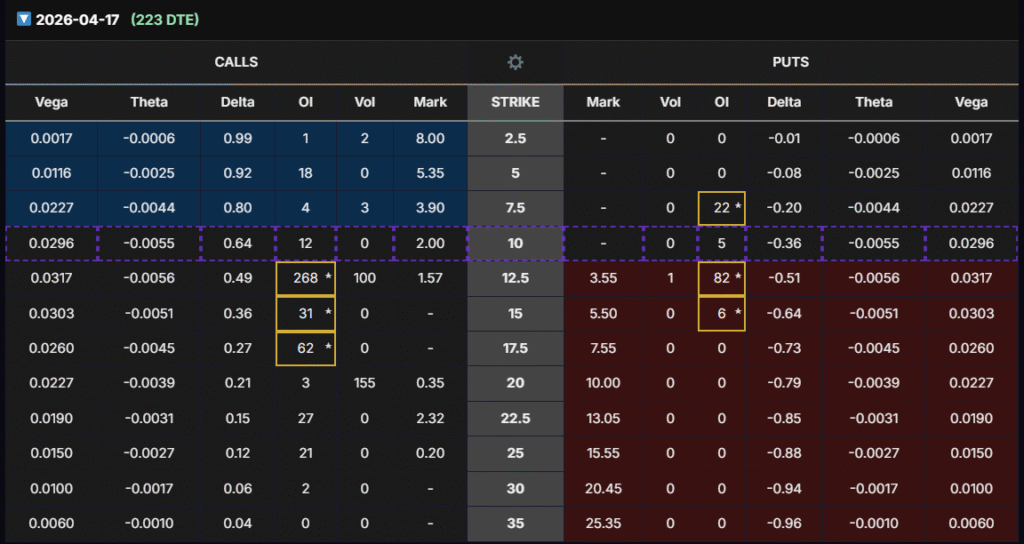

- Apr 2026 (223 DTE) expiration: Clearer bullish skew emerges. The $12.5 strike calls carry the strongest liquidity (268 OI), balanced delta (~0.49), and high Vega exposure. Put interest is much lighter, showing that traders are less focused on downside protection at this horizon.

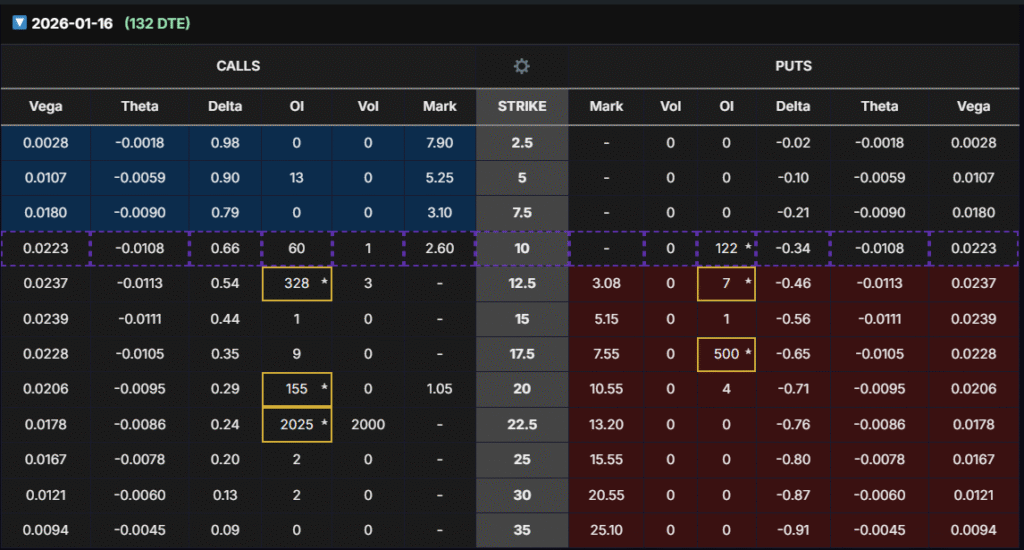

This shift from short-term hedging to longer-term upside positioning implies the market expects SPRY to stabilize and potentially recover into 2026.

🎯 LEAPS Strategy Setup

After reviewing the 223 DTE chain, the best candidate for a LEAPS trade is:

- Contract: Apr 17, 2026 $12.5 Call

- Delta: ~0.49 → right at the sweet spot (~0.50).

- Vega: 0.0317 → highest among near-the-money strikes, offering strong sensitivity to IV expansion.

- Open Interest: 268 → the most active strike in this expiration, ensuring liquidity.

This contract strikes the perfect balance between price participation (delta), implied volatility exposure (vega), and tradability (OI). At ~$10 stock price, the $12.5 strike is just out-of-the-money, offering leverage without being overly speculative.

If SPRY moves toward analysts’ $18–$22 price targets, the $12.5 call would transition deep in-the-money, generating strong delta gains. Combined with an IV spike around earnings or FDA catalysts, this setup gives multiple profit pathways — making it the most attractive LEAPS candidate.

📌 Final Takeaways

- Technicals: Oversold with bearish momentum — support at $9.50–$10 is critical.

- Financials: Strong balance sheet, high margins, but ongoing losses and dilution risk.

- Analyst Targets: Consensus bullish, with upside ranging from +80% to +200%.

- Insider Activity: Heavy selling near highs, no recent insider accumulation.

- Options Flow: Neutral near-term, bullish long-term.

- LEAPS Play: Jan 2026 $12.5 Call is the optimal contract for exposure.

⚠️ Disclaimer

This analysis is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell securities.