Technical Chart Review

Kenvue (KVUE) has now reached fresh multi-timeframe lows:

- 3-Month Chart: KVUE touched a 3-month low near $16.97, with steep declines across September. The RSI is oversold (~25), and MACD shows a bearish crossover. While oversold conditions often produce technical bounces, momentum is still firmly bearish.

- 1-Year Chart: KVUE is sitting at a 1-year low. RSI is at ~26, confirming extended oversold conditions. The MACD confirms bearish momentum, widening further. Volume spikes suggest capitulation selling pressure.

- All-Time Chart: KVUE is at an all-time low, breaking below key supports without historical price memory. RSI (~28) signals rare extended oversold levels, while MACD confirms structural weakness.

✅ Takeaway: Oversold across all timeframes, yet momentum remains bearish. Short-term relief rallies may occur, but KVUE is in a “falling knife” phase where staged accumulation strategies are required.

Financials Overview

Kenvue’s fundamentals tell a more nuanced story beneath the panic-driven selloff:

- Revenue Strength:

- Total revenue (TTM): $15.14B

- Gross profit: $8.80B → 58.1% gross margin, showing strong pricing power for branded consumer health products.

✅ Interpretation: Healthy topline, consistent with a stable consumer staples company.

- Profitability:

- Operating margin: 17.5%

- Net margin: 9.4%

✅ Interpretation: Gross margin is excellent, but net margin drops off due to high SG&A and marketing costs. This is typical for consumer healthcare, but it highlights efficiency risks compared to peers like Procter & Gamble (PG).

- Earnings:

- EPS (TTM): $0.74

- EPS (FQ): $0.22

✅ Interpretation: Modest earnings base, reflecting a defensive but not high-growth profile.

- Cash Flow:

- Operating cash flow (TTM): $2.09B

- Free cash flow (TTM): $1.63B

- CapEx (TTM): $464M

✅ Interpretation: Strong free cash flow generation in the billions — a major cushion for dividends, debt servicing, and stability during downturns.

- Balance Sheet Strength:

- Debt-to-equity ratio: 0.81 → relatively low leverage.

- Total debt: $8.74B vs equity: $10.73B → balanced capital structure.

✅ Interpretation: Low risk of debt distress, especially with strong FCF support.

- Efficiency & Returns:

- ROE: 13.6%

- ROIC: 8.1%

- ROA: 5.3%

✅ Interpretation: Returns are respectable but not elite. This reflects KVUE’s position as a steady defensive play, not a hyper-growth company.

- Dividends:

- Dividend yield: 4.53% (annual payout $0.81/share).

- Payout ratio: 111% (TTM) → dividends are technically stretched relative to earnings.

✅ Interpretation: Dividend is attractive, but the payout ratio signals management is leaning heavily on FCF to sustain it.

- Valuation Multiples:

- P/E: 24.9

- P/CF: 16.9

- EV/EBITDA: 13.1

✅ Interpretation: Valuation is not deep-value cheap, but the stock is trading at historic lows relative to its fundamentals and analyst targets.

Financials Takeaway

KVUE is financially solid, cash-generating, and low-debt, making it a defensive consumer staples name. The key issues are low net margins and a high payout ratio, which weigh on growth prospects. However, the company’s $1.6B+ in free cash flow, 58% gross margin, and low leverage create a strong floor beneath the current fear-driven selloff.

✅ Investor View: At all-time stock lows, KVUE’s financials highlight that the company is undervalued relative to its stability and cash flow strength. This supports the case for second-batch options entry, as downside risk is more sentiment-driven than balance sheet-driven.

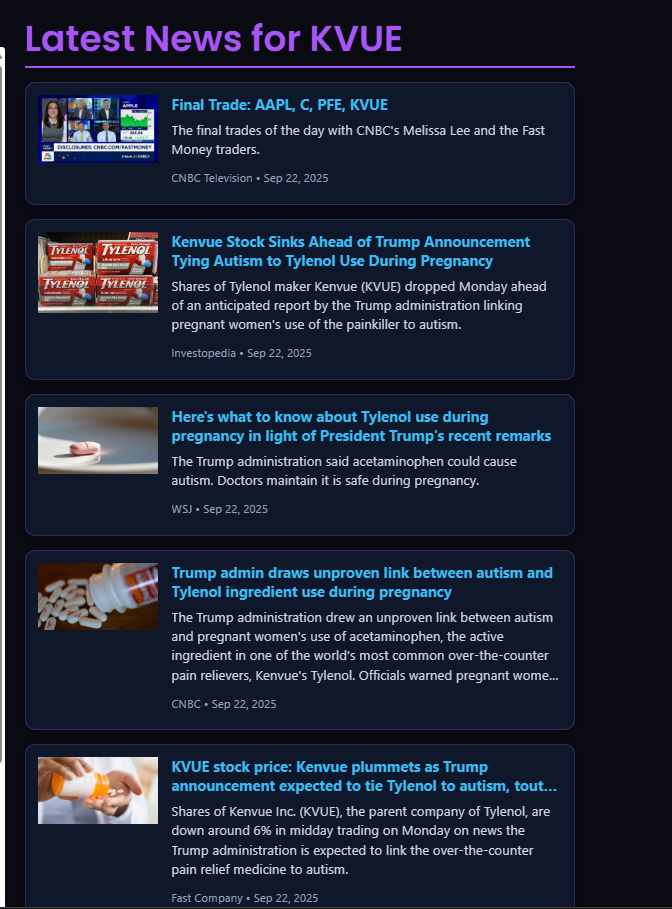

News Catalyst

The latest selloff ties directly to Trump administration remarks suggesting a potential link between Tylenol use during pregnancy and autism. While major outlets (WSJ, CNBC) called the link “unproven,” the fear of litigation and regulatory overhang triggered a steep selloff.

✅ Takeaway: Headline risk is driving panic. No new scientific evidence has been presented, yet the market has priced in worst-case litigation outcomes.

Analyst Price Targets

Recent analyst actions highlight upside:

- Barclays: $23 target (raised from $21).

- Canaccord: $29 target (raised from $24).

- Jefferies: Initiated Buy with $27 target.

- RBC Capital: $24, downgraded to Sector Perform.

- Bernstein: Bearish outlier with $18 target.

✅ Consensus: Targets cluster between $21–27, suggesting 30–60% upside from current levels ($17). Even bearish estimates sit above today’s price.

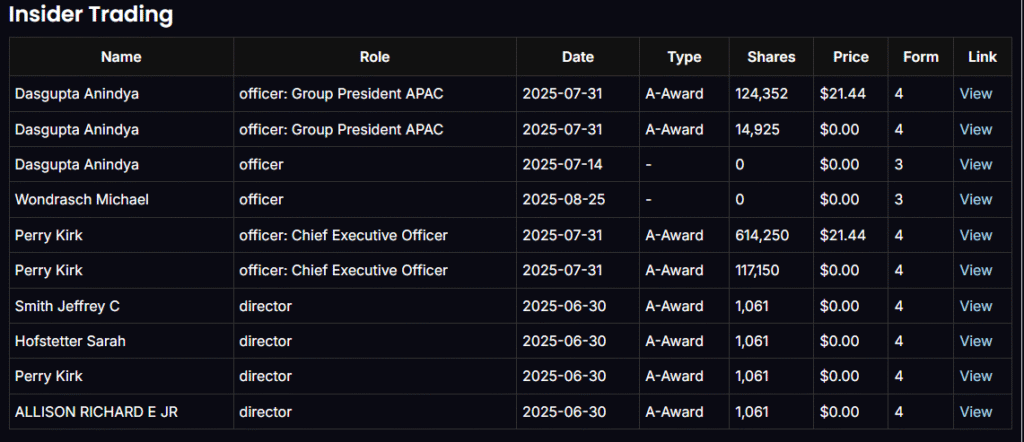

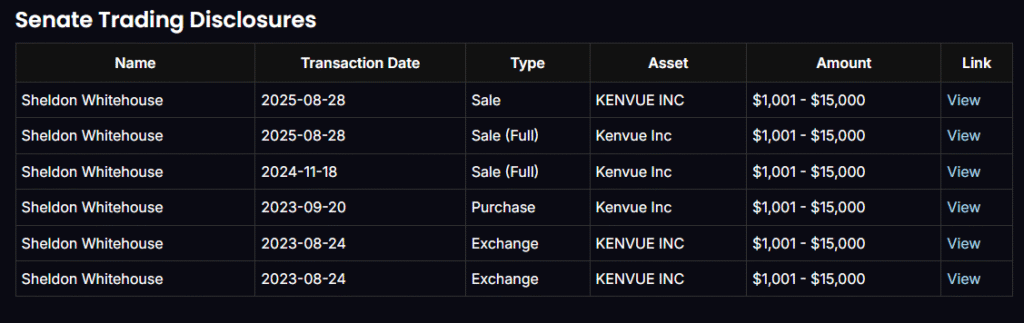

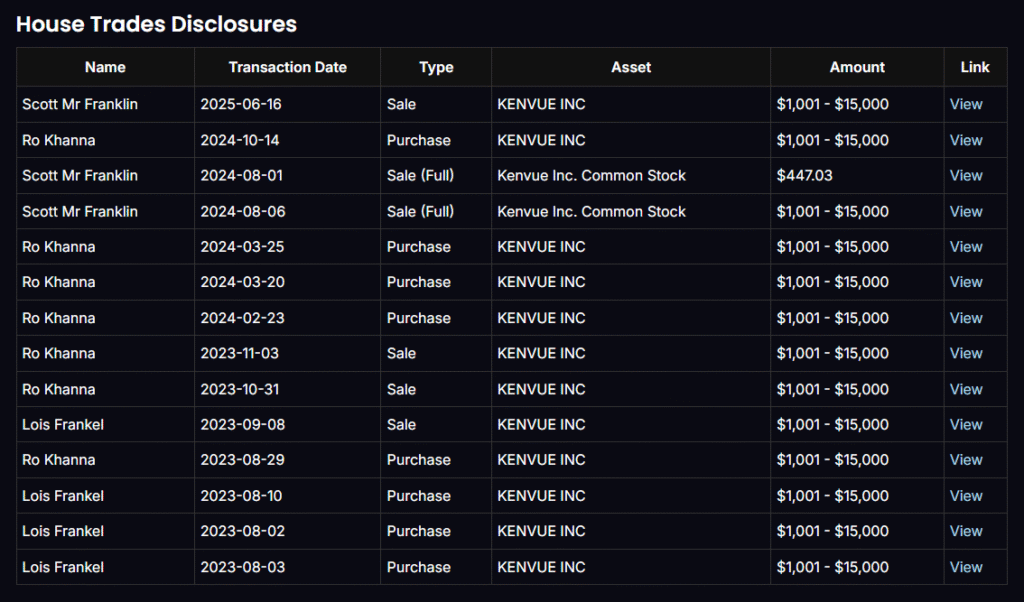

Insider & Political Trading

- Executives: CEO Kirk Perry received 614k shares at $21.44 via awards. No insider dumping has occurred. This signals management confidence in long-term value.

- Senate/House Trades: Mixed — Sen. Whitehouse trimmed exposure, while Rep. Ro Khanna made multiple purchases. Some politicians exited fully (Scott Franklin), but insiders remain committed.

✅ Takeaway: Insiders are aligned with shareholders, while politicians are mixed. No red-flag insider selling.

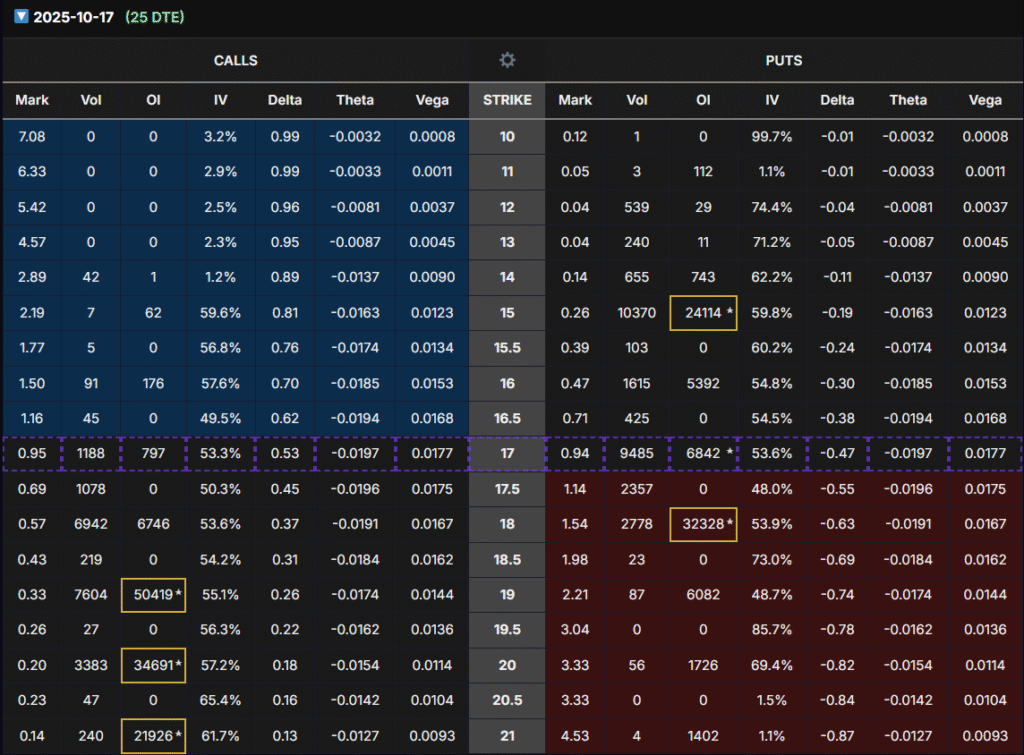

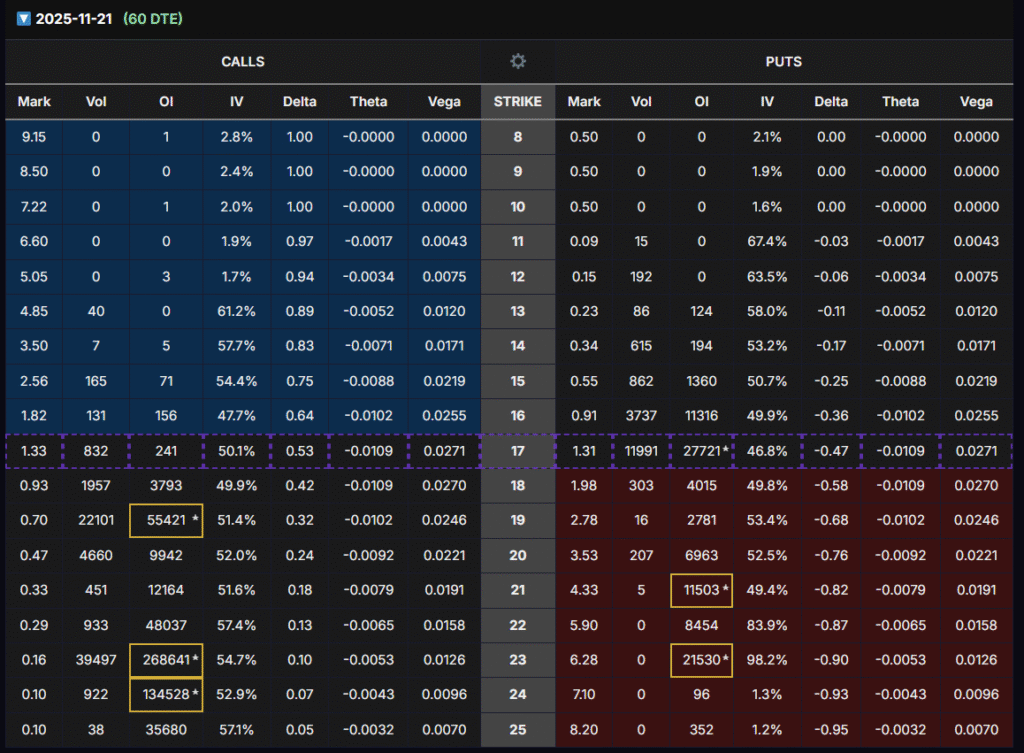

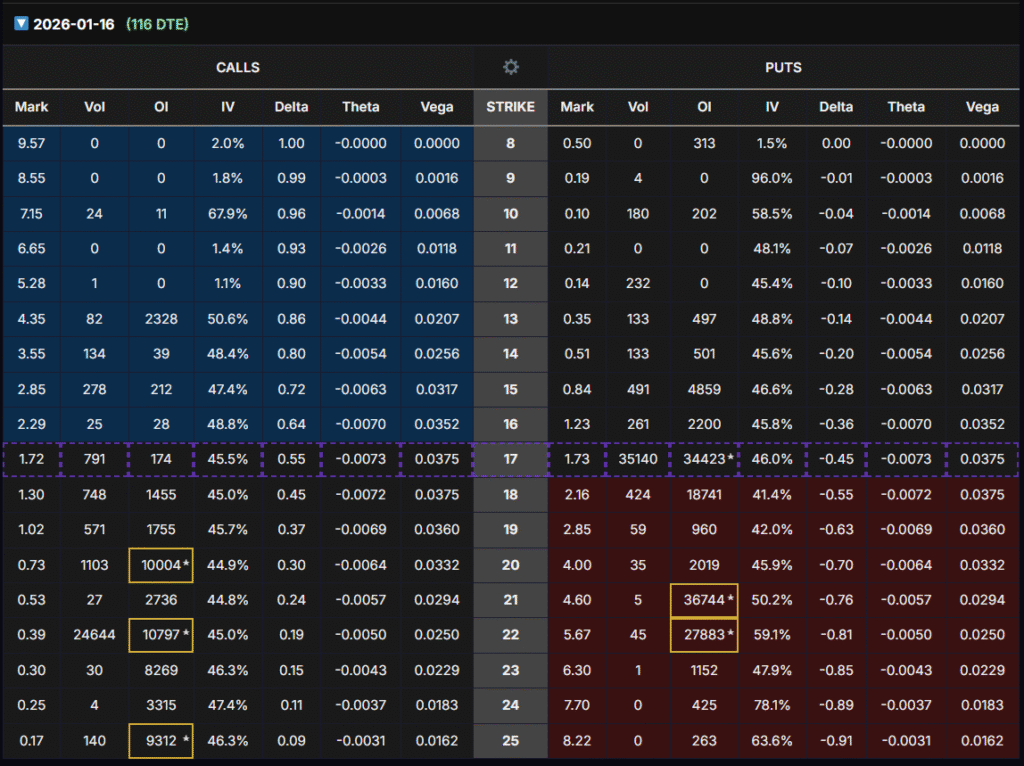

Options Flow Analysis

- Short-Term Flow (25–60 DTE): Heavy call OI stacked at $19–23 strikes, far above current price. Suggests speculative bullish bets for medium-term recovery.

- Longer-Term Flow (Jan 2026 LEAPS): Strong clustering at $20–25 strikes. This aligns with analyst targets.

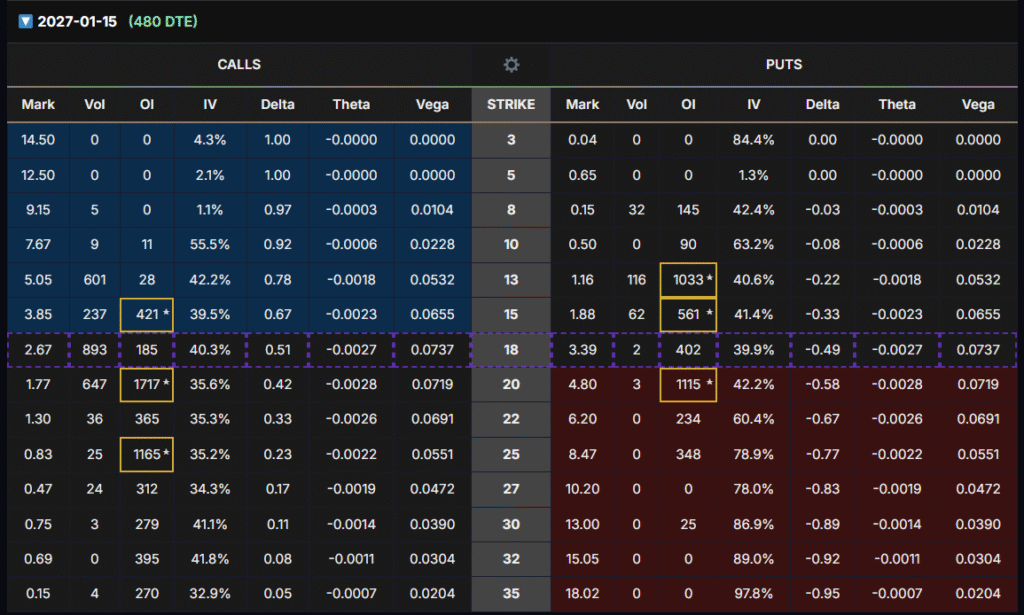

- Current Chain (Jan 2027, 480 DTE):

- Strike $20C → OI 1,717 contracts (highest on call side).

- Delta ~0.42, Vega ~0.072.

- This strike balances leverage, liquidity, and volatility sensitivity.

✅ Takeaway: Call flow shows speculative accumulation in OTM strikes. The $20C LEAPS stands out as the most optimal choice for a pre-earnings Vega/Delta strategy.

Strategy: Second Batch Entry

We are now moving into our second batch entry because:

- The options price has dropped -40% to -50% from our first batch entry, aligning with our staged accumulation plan.

- Earnings are 1 month away, which means implied volatility and Vega will expand sharply in the run-up.

- Our focus is not on the stock reaching $20 immediately, but on selling Vega at a premium before earnings.

- Target: Close right before earnings to capture 80–130% gains (conservative).

- Why it works: If KVUE stock even moves up 10%, our $20C contracts (delta ~0.4) could move 3–5x faster due to Delta + Vega.

- Risk Management: If after 2 months profits have not materialized, we must roll over into a later-dated strike to avoid stagnation.

Batch Entry Instructions

- First Batch: Enter at current levels (done).

- Second Batch: Enter when the options price drops -40% to -50% from first batch cost (now).

- Third Batch: Enter when the options price of the second batch drops -40% to -50% further.

Important: These drops refer to the options price, not the stock price.

Risk Management Disclaimer

This analysis is for informational purposes only. Options trading involves high risk and is not suitable for all investors.

- Allocate only 2% of total portfolio capital to this KVUE strategy.

- Holding period should be capped at 2 months maximum, with rollovers as needed.

- Always close positions before earnings to avoid IV crush.

✍️ Final Word:

KVUE’s stock is oversold, headlines have triggered panic, but financials remain sound. With analysts projecting 30–60% upside and options flow heavily stacked at $20–25 strikes, our second batch entry into the KVUE Jan 2027 $20C LEAPS is strategically timed to capture volatility expansion ahead of earnings.