Setup date: Oct 3, 2025 • Focus: Buy-vega / buy-delta LEAPS, exit before earnings IV crush

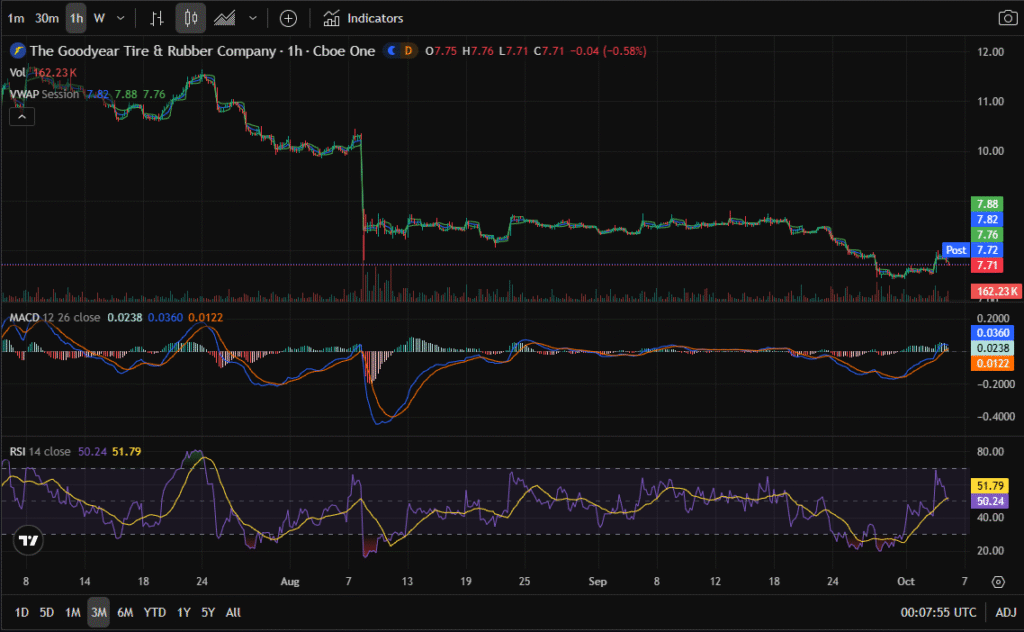

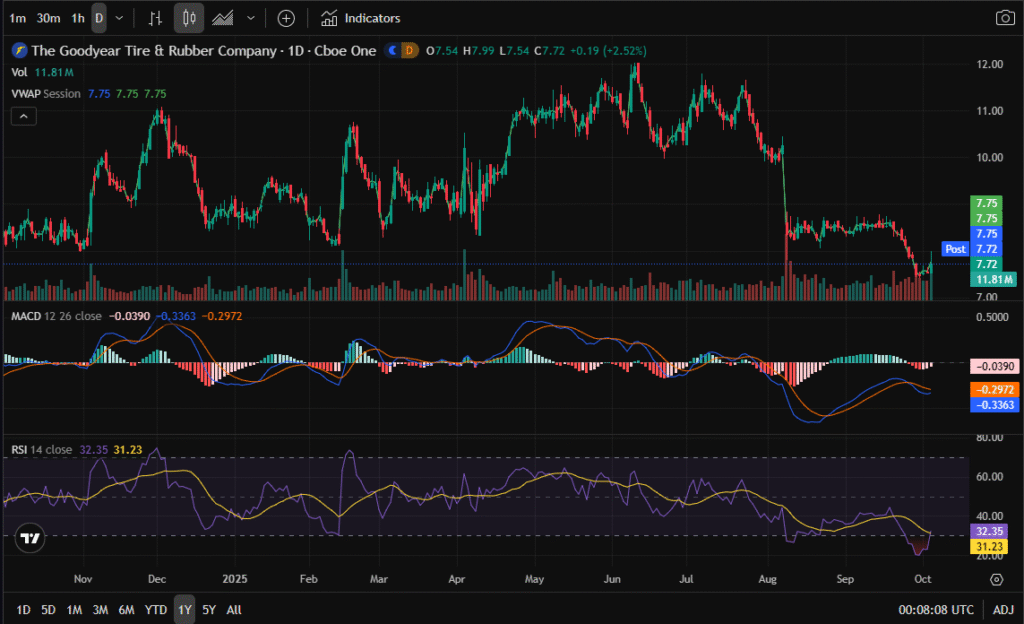

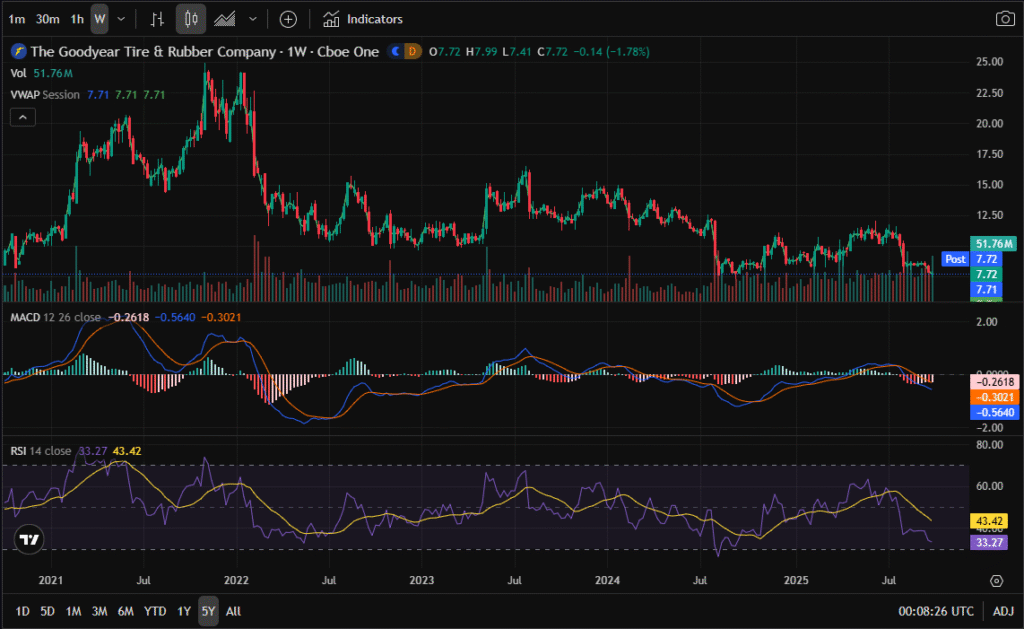

Quick technical read (why now)

- 3M : New 3-month lows with steep drops. RSI ~50 (stabilizing), MACD bullish crossover → scope for a short-term bounce.

- 1Y : 52-week low zone. RSI oversold ~32, MACD still bearish → trend weak but stretched.

- 5Y : Retesting pandemic-era lows; RSI oversold, MACD bearish → secular pressure persists.

Implication: We’re not chasing a long-term equity reversal. We’re setting up a volatility (vega) + price sensitivity (delta) trade that profits from the pre-earnings IV run-up, with minimal theta drag thanks to long DTE.

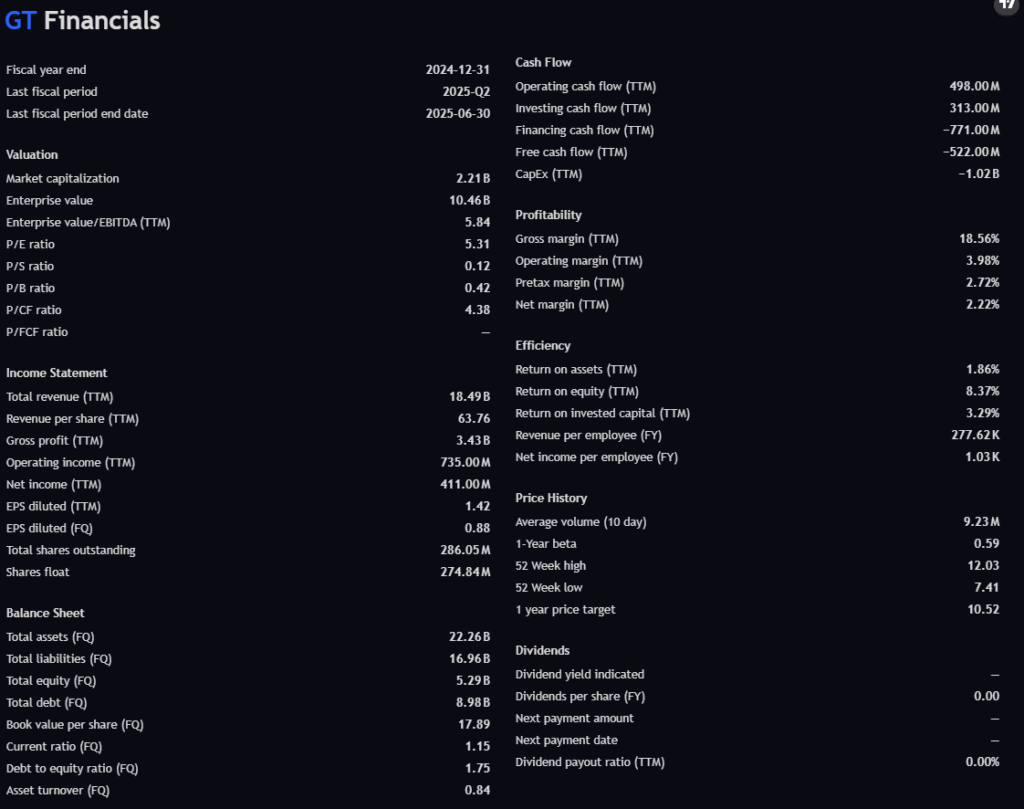

Financials snapshot (what the numbers say)

From your sheet (TTM / latest Q2 FY2025):

- Revenue: $18.49B (no strong topline momentum).

- Margins: Gross 18.56%, Operating 3.98%, Net 2.22% → razor-thin; modest shock can erase profits.

- Cash Flow: FCF –$522M (OCF $498M – CapEx ~$1.02B) → negative free cash flow is the core risk.

- Returns: ROE 8.37%, ROIC 3.29% (< likely WACC) → value creation questionable.

- Balance sheet: Debt/Equity 1.75, book value $17.89/sh, P/B 0.42 → optically cheap but leveraged.

- Price context: 52-week $7.41–$12.03; average PT on your panel $10.52.

Takeaway: Fundamentals are “cheap for a reason.” This favors a pre-catalyst IV trade over a buy-and-hold equity position.

News flow (does it move the needle?)

Recent headlines skew brand/PR (Snoopy blimp, Ice Cube tour, awards) plus a motorsport reorg. These support brand equity but are not margin or FCF fixes. The lone substantive angle in your feed is a post-earnings contrarian bull note arguing headwinds are temporary. Net-net: no concrete hard catalysts yet beyond the next earnings cycle—exactly why we monetize IV expansion into earnings rather than post-earnings fundamentals.

Analyst targets (sentiment trend)

- Aug 8, 2025 – BNP Paribas: $9 (Neutral) — ~7–15% upside from here; cautious.

- Jun 13, 2024 – Morgan Stanley: $14 (Equalweight).

- Older (2022): $15–$19 targets (higher conviction then).

Read: Street targets trended down over time. Today’s targets still sit above spot, but conviction is muted—again favoring short window, pre-earnings IV trade over long-dated fundamental bet.

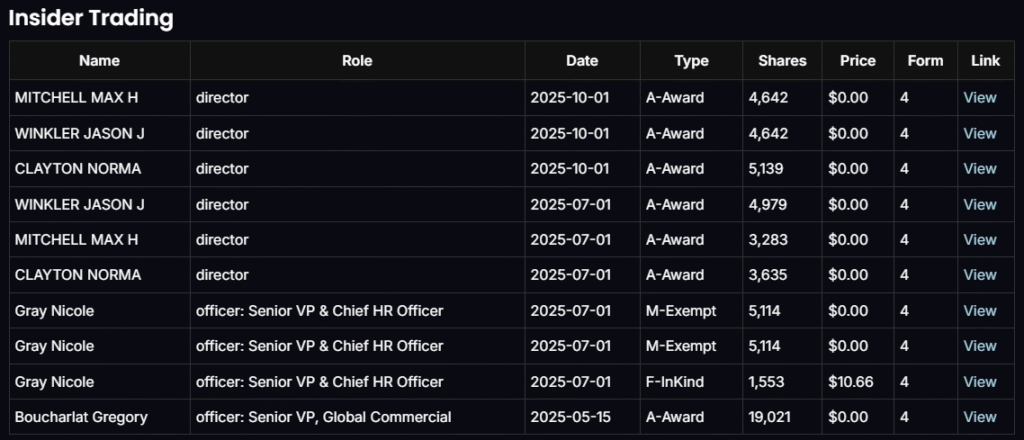

Insider activity (conviction check)

Your Form 4 panel shows A-Awards/M-Exempt/F-In-Kind grants/vests for directors and officers; no recent open-market insider buys at depressed prices. That’s not a bullish conviction signal and reinforces using a tactically defined options window instead of a thesis that requires insider-aligned turnaround timing.

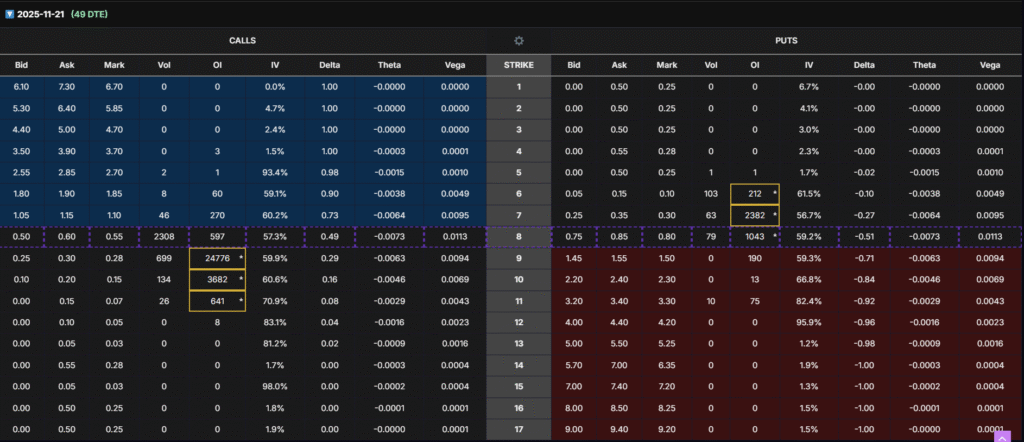

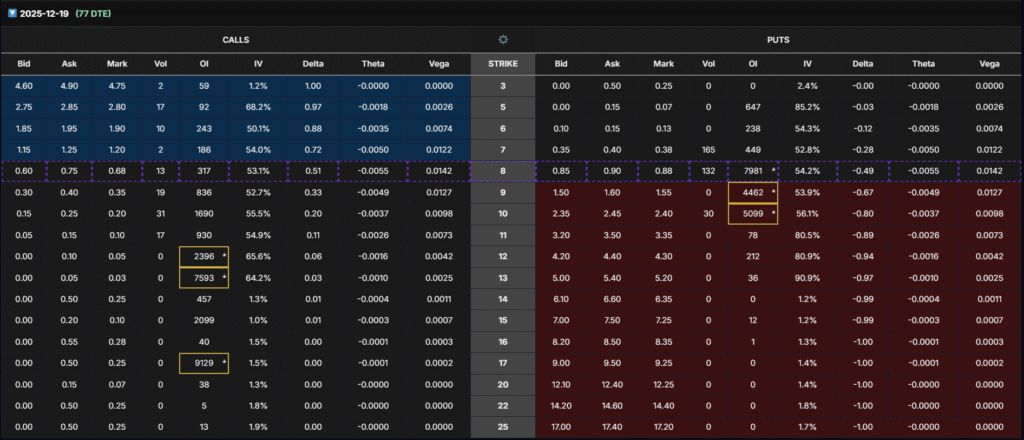

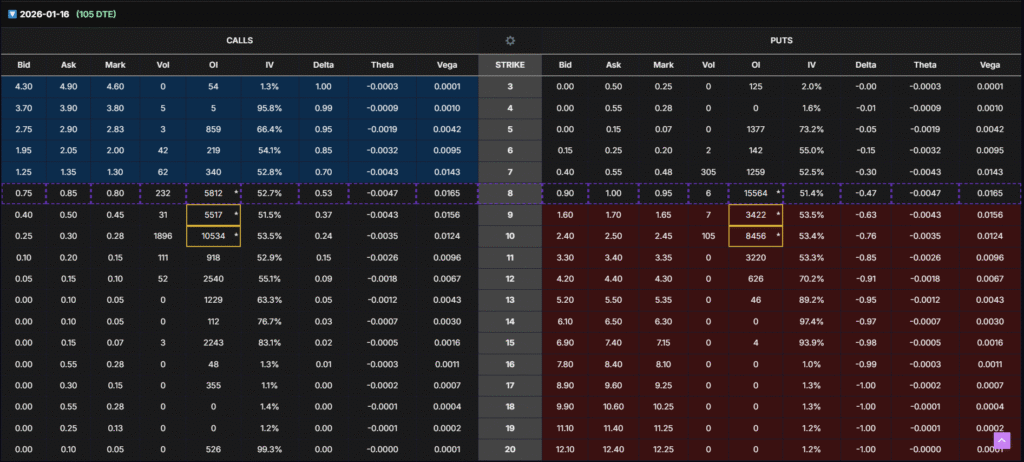

Options flow (calls) — what traders are signaling

Near-dated clusters:

- Nov ’25 (49 DTE): $8C OI ~24,776; $9C OI ~3,682 → short-term bounce bets around/above $8.

- Dec ’25 (77 DTE): $12C OI ~9,129, $13C ~7,593 → speculative upside farther OTM.

- Jan ’26 (105 DTE): $10C OI ~10,534, $9C ~5,517, $8C ~5,812 → balanced ATM/OTM upside interest.

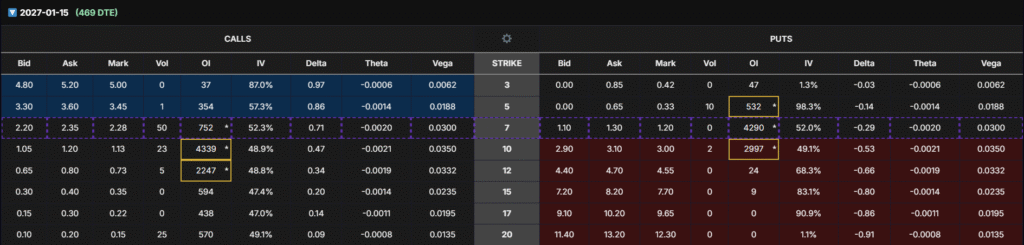

LEAPS (anchor for our trade):

- Jan 15, 2027: $12C OI ~2,247, Delta ~0.34, Vega ~0.033; $10C larger OI but Delta ~0.47 (less “cheap vega”).

Read: Skew is bullish-speculative on calls, with meaningful interest at $10–$13 into winter/early-’26. For our purpose, the $12C Jan ’27 offers the best vega per dollar at a target delta.

The trade — buy vega cheap, sell vega dear (exit before IV crush)

Contract: GT Jan 15, 2027 $12 Call (≈469 DTE)

- Why this strike: Delta ~0.34 (3–4× stock sensitivity), high OI/liquidity, higher vega than deeper OTM peers.

- What pays us:

- IV run-up into the next earnings/catalyst (vega pop), and

- Any +5–10% stock bounce (delta).

- What we avoid: Holding through earnings (post-event IV crush).

Holding window: Max 2 months. If targets aren’t reached, roll to the next cycle to keep vega exposure fresh and avoid dead money.

Entries, exits, and scaling plan

Initial Entry (Batch 1): Buy now while IV is relatively low.

Profit management:

- Base target: +80%.

- At +80%, you may close 2/3 of the position and leave 1/3 to pursue 100–110%+ (stretch).

- Hard stop/time stop: If not working by 2 months, roll rather than linger.

Three-Batch Scaling (very explicit on triggers):

- Batch 1 — Today.

- Batch 2 — In 1–2 weeks only if the options price of Batch 1 is down –40% to –50% (this is about the options price, not the stock).

- Batch 3 — Another 1–2 weeks later only if the options price of Batch 2 declines –40% to –50%.

This keeps risk modular and exploits cheaper vega if the market drifts.

Risk budgeting & housekeeping

- Position sizing: ≤2% of total portfolio per batch (max 6% if all three batches fill).

- Respect liquidity; use limits and spread the fills.

- Exit before the earnings date to crystallize the IV expansion and sidestep event risk.

Bottom line

GT is a classic “cheap but risky” fundamental story. Rather than argue with the balance sheet, we exploit how options are priced: buy long-dated $12C LEAPS for vega at depressed IV, let delta help on any bounce, and exit before earnings to sell that pumped IV back to the market. With tight 2-month max hold, explicit –40% to –50% options-price scaling, and 2% per batch sizing, this is a controlled, rules-based way to monetize GT’s oversold setup without requiring a long-term turnaround.

Disclaimer (read this)

This content is for educational and informational purposes only and is not investment advice. Options are risky and can result in total loss. Use position sizing ≤2% of total portfolio per batch (max 6% across three batches). Triggers referencing declines of –40% to –50% apply only to the options price, not the stock price. Always evaluate liquidity, bid/ask spreads, and personal suitability. Past performance does not guarantee future results.