🔹 Introduction

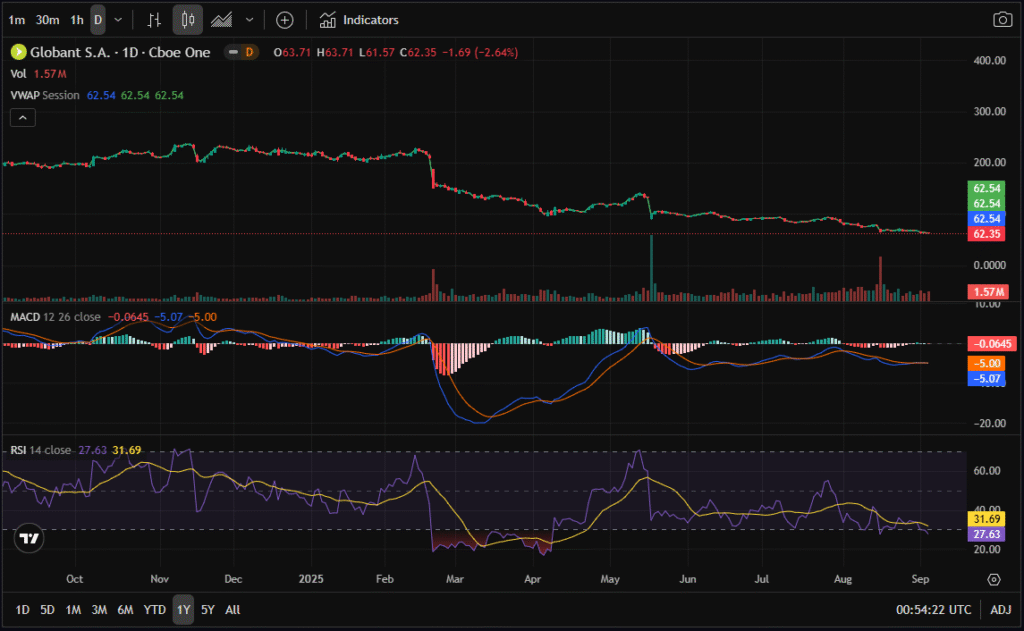

Globant S.A. (Ticker: GLOB) has been a consistent player in the digital IT services sector, but as of today, its stock trades at a striking five-year low of $62.35. For long-term investors, this looks like a dramatic fall from grace, given that the stock once commanded prices above $200. For options traders, however, this extreme dislocation may present a high-risk, high-reward setup.

By combining a technical read, financial analysis, and an options chain review, this article makes the case for a LEAPS strategy targeting Vega and Delta gains while keeping Theta decay negligible. With the plan to exit before earnings in the coming months, the trade is speculative but offers compelling upside potential.

🔹 Technical Analysis

From a chart perspective, GLOB is undeniably in bear market territory. The stock has been in a prolonged downtrend, consistently making lower highs and lower lows.

- RSI (Weekly): Around 27, firmly oversold, which historically has coincided with technical bounces.

- MACD: A bearish crossover occurred last month and momentum remains negative.

- Volume: Elevated during down days, signaling institutional selling pressure.

Interpretation: The chart screams caution. GLOB is a “falling knife,” but with oversold readings on multiple timeframes, the conditions for a relief rally are forming. For short-term traders, this is precisely the kind of setup where oversold bounces can provide meaningful gains.

🔹 Fundamentals Snapshot

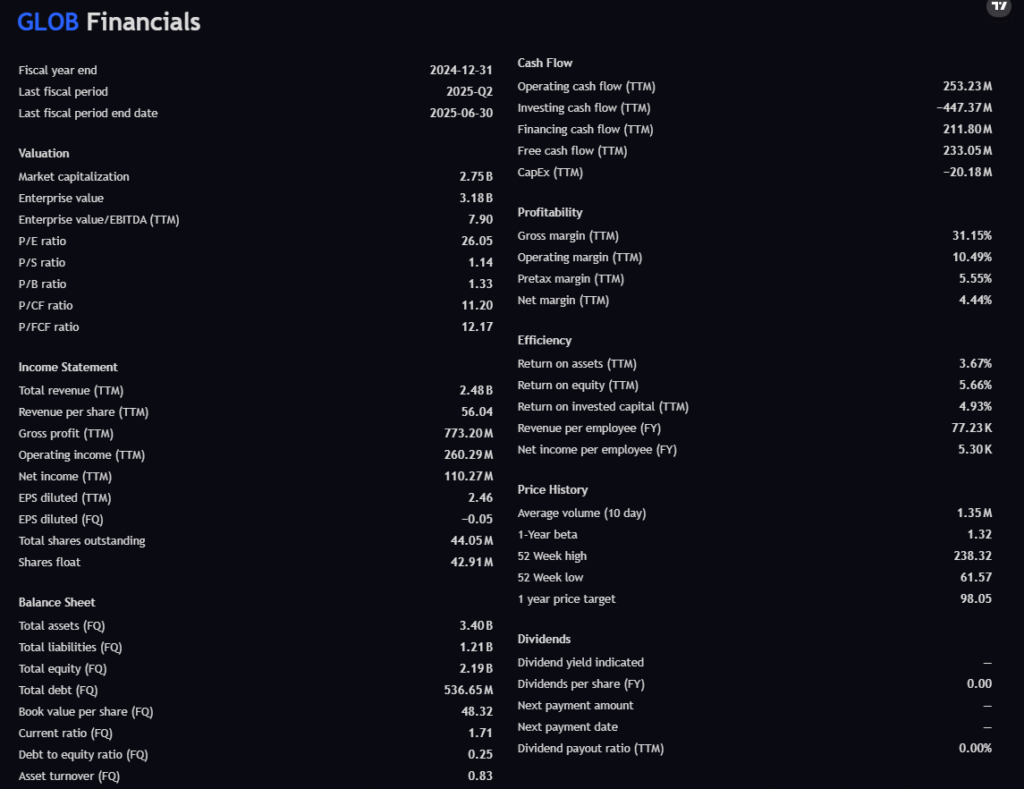

Despite the ugly chart, Globant’s financial profile shows both strengths and weaknesses.

- Revenue (TTM): $2.48 billion, with gross profit of $773 million.

- Free Cash Flow (TTM): $233 million → positive and healthy.

- Debt-to-Equity: 0.25 → low leverage and financial resilience.

- Gross Margin (31%): Acceptable for an IT services company, but not in elite SaaS territory.

- Net Margin (4.4%): Weak — this is the real red flag. Peers often generate 10–15% net margins.

- ROE (5.7%) & ROIC (4.9%): Low, suggesting limited efficiency in converting revenue into shareholder value.

- Valuation: EV/EBITDA (7.9) and P/FCF (12) suggest undervaluation on cash-flow metrics, even as P/E (26) looks expensive relative to earnings growth.

Interpretation: The company is financially stable, cash-flow positive, and has low debt, but suffers from thin profitability and weak returns. Investors clearly lack confidence in margin recovery, which helps explain the severe share price collapse.

🔹 Analyst Sentiment

Analysts are still largely bullish despite trimming expectations:

- Most recent targets (2025): $153 from Mizuho, $160 from Susquehanna.

- Higher estimates: Jefferies at $255, Needham at $265.

- Median target: Around $200, implying +220% upside from current levels.

Even after multiple downward revisions, the lowest target remains more than 2x the current price. The gap between analyst models and market sentiment is massive.

Interpretation: Analysts see Globant as oversold, but the market demands proof of profitability improvements before re-rating the stock.

🔹 Options Chain & LEAPS Setup

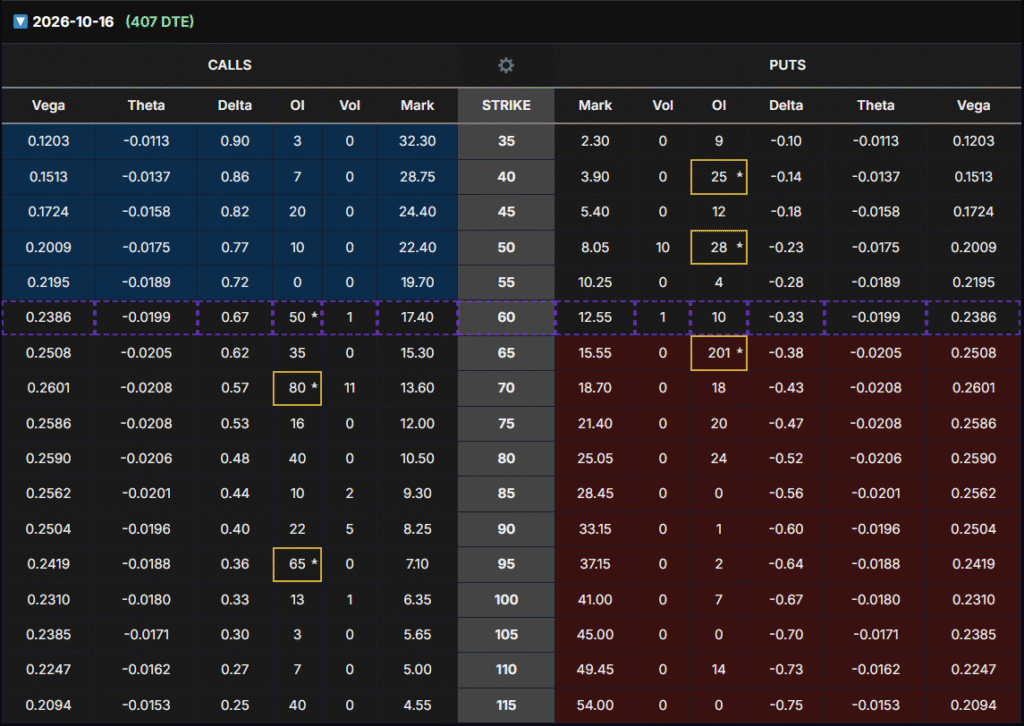

To take advantage of this setup, we analyze the October 2026 expiration (407 DTE):

- $80 Call Selected:

- Delta = 0.48 (sweet spot between 0.45–0.50).

- Vega = 0.2590 (highest among strikes).

- Theta = -0.0206 (time decay negligible).

- Premium = ~$10.50 ($1,050 per contract).

This strike is optimal because it provides balanced Delta exposure while maximizing Vega sensitivity. The strategy is not to hold until 2026, but rather to exit 1 day before earnings when implied volatility typically peaks.

🔹 Profit Scenarios

- If stock rebounds to $75 (+20%): Option could rise 40–60% from Vega expansion plus Delta gains.

- If stock rallies to $90 (+45%): Option could double or triple in value (+150–200%).

- If stock trades flat ($62–65): Theta loss is minimal, and Vega expansion may still generate a small profit.

- If stock drops to $50: Option value could decline to ~$7–8, a -25–30% loss.

🔹 Risk/Reward Balance

- Upside: +100–200% if GLOB rebounds and IV rises into earnings.

- Downside: -25–40% if bearish momentum continues.

- Risks: Weak profitability, no technical support below current levels, limited liquidity in options chain.

🔹 Investment Thesis

Globant is not a safe long-term investment at this stage due to profitability concerns and technical weakness. However, for a short-term options trader, it presents a compelling setup:

- Technicals: Deeply oversold, with the potential for a rebound.

- Fundamentals: Strong free cash flow and low debt provide a safety cushion.

- Analysts: Even the most bearish estimates see the stock far higher than today.

- Options Play: Long-dated calls allow traders to exploit Vega expansion into earnings while keeping Theta minimal.

✅ Conclusion

The Oct 2026 $80 Call is a strategic way to play Globant’s oversold condition. By targeting Vega gains and Delta movement, traders can position for a speculative bounce and exit before earnings to avoid IV crush.

This is a high-risk, high-reward play that should be sized conservatively. It is not a core portfolio investment but rather a tactical trade that leverages both technical oversold conditions and options pricing dynamics.

At current levels, Globant is a speculative LEAPS buy for options traders, with the plan to sell into strength before earnings season.

⚠️ Disclaimer

This article is for educational and informational purposes only and should not be taken as financial advice. Options trading involves significant risk and may not be suitable for all investors.