1️⃣ Technical Analysis (3-Month, 1-Year, and 5-Year Charts)

Chipotle Mexican Grill (NYSE: CMG) has entered a rare technical setup across multiple timeframes, combining deep oversold readings with a potential volatility rebound.

- 3-Month Chart: CMG has printed a steep three-month decline, now forming a potential base near $30.40, a level representing a capitulation low. The MACD recently made a bullish crossover, and the RSI sits near 34, suggesting the short-term selling momentum is fading.

- 1-Year Chart: The one-year view confirms a downtrend, but the RSI is extremely oversold (18.59) — a level that historically precedes multi-week rebounds for CMG.

- 5-Year Chart: The longer horizon shows the stock testing a multi-year support around $30, last touched in early 2021. This area aligns with a high-probability reversal zone where institutional accumulation often begins.

Technically, CMG is deeply compressed and coiled, making it ideal for a volatility expansion play using LEAPS calls.

2️⃣ Financial Analysis

Despite the technical weakness, CMG remains financially robust.

- Revenue (TTM): $11.79B

- Free Cash Flow: $1.57B

- Net Margin: 13.04%

- ROE: 44.96%

- Operating Cash Flow: $2.21B

Even after the selloff, CMG maintains elite fundamentals with strong profitability and efficiency. Its debt-to-equity ratio (1.55) is higher than historical norms but still manageable given its free cash generation.

Overall, CMG’s valuation compression (P/E 26.9) makes it an undervalued growth name relative to its historical premium.

3️⃣ Latest News Headlines & Sentiment

Recent headlines suggest a mix of institutional repositioning and new strategic initiatives:

- Positive Catalysts:

- Chipotle Launches “Chipotle U Rivalry Week” — a marketing push aimed at reigniting demand among younger consumers.

- CMG Signs Multi-Year Simulation Software Licensing Agreement — emphasizing operational efficiency through digital innovation.

- Institutional Pressure:

- Several funds (American Century, Virtus SGA) trimmed CMG in Q3 due to short-term performance drag, yet most retained their long-term exposure — signaling confidence beyond this correction phase.

Sentiment Summary: Short-term neutral, long-term bullish — corporate innovation and efficiency investments continue to support the brand’s fundamental moat.

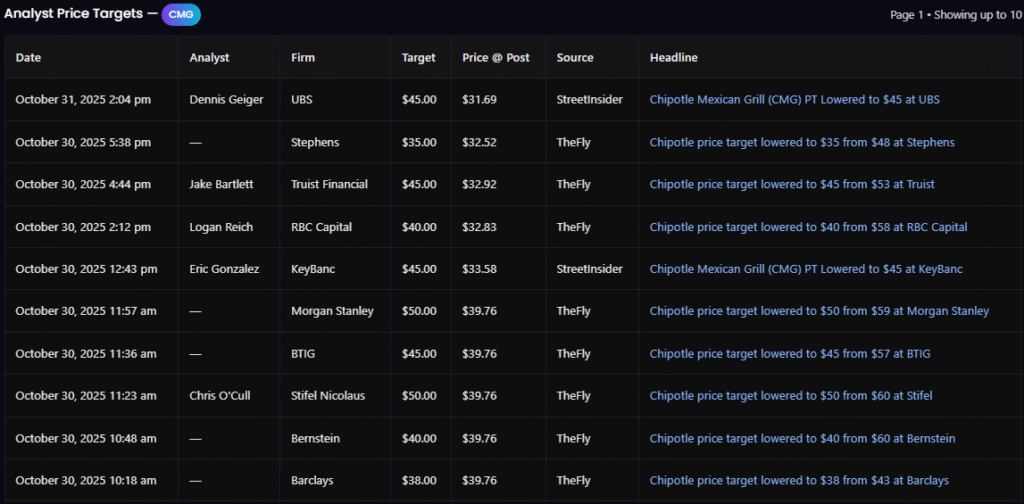

4️⃣ Analyst Price Targets

Across 10 major firms in late October, analyst targets now range from $35 to $50, with an average of $43.7, implying ~40% upside from current levels.

- Morgan Stanley / Stifel: $50 (Bullish)

- UBS / Truist / KeyBanc: $45 (Neutral-Positive)

- Stephens / RBC / Bernstein: $35–$40 (Cautious)

Importantly, no major analyst has downgraded CMG to a “Sell.” Instead, all have simply reset targets, which historically signals a capitulation point rather than ongoing pessimism.

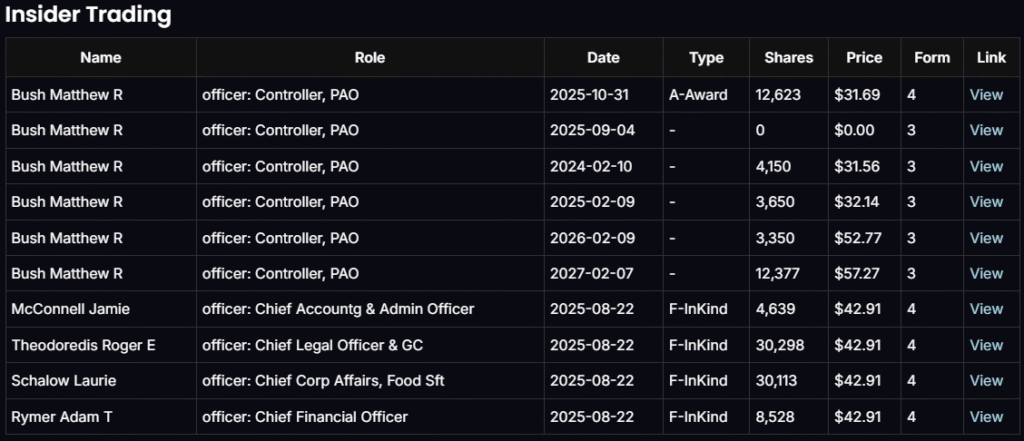

5️⃣ Insider & Political Trades

Corporate Insiders:

Recent Form 4 filings show no insider selling. Executives such as the CFO and Chief Legal Officer received equity grants at prices near $31–33, demonstrating continued internal confidence.

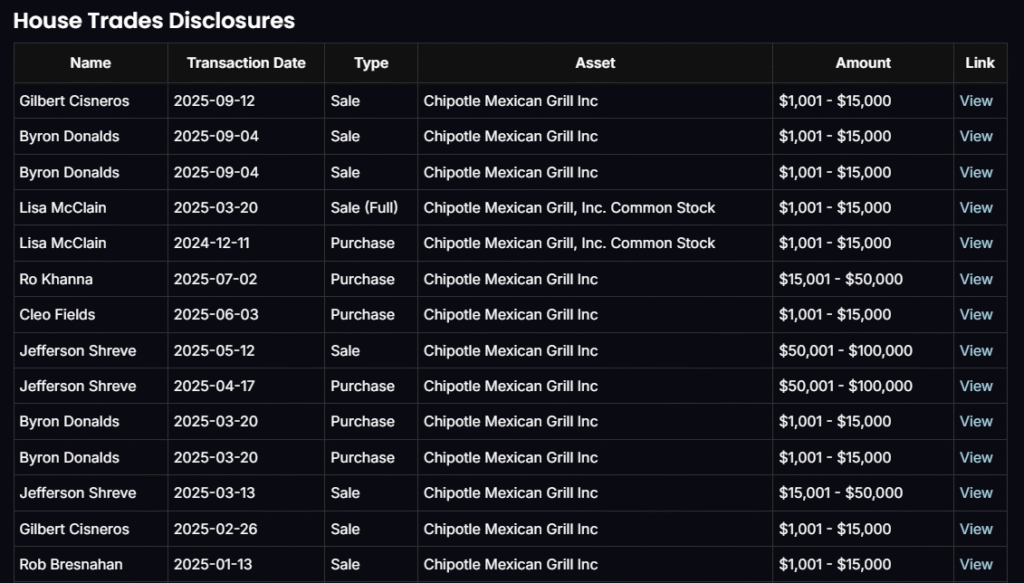

Senate & House Disclosures:

While Senator John Hickenlooper had previously trimmed his CMG holdings earlier in 2025, no new sales occurred after the correction. Notably, multiple House representatives — including Ro Khanna and Cleo Fields — purchased shares in mid-2025, near current price levels.

Interpretation: Insider and political sentiment remains neutral-to-bullish, reinforcing the idea that institutional selling exhaustion is complete.

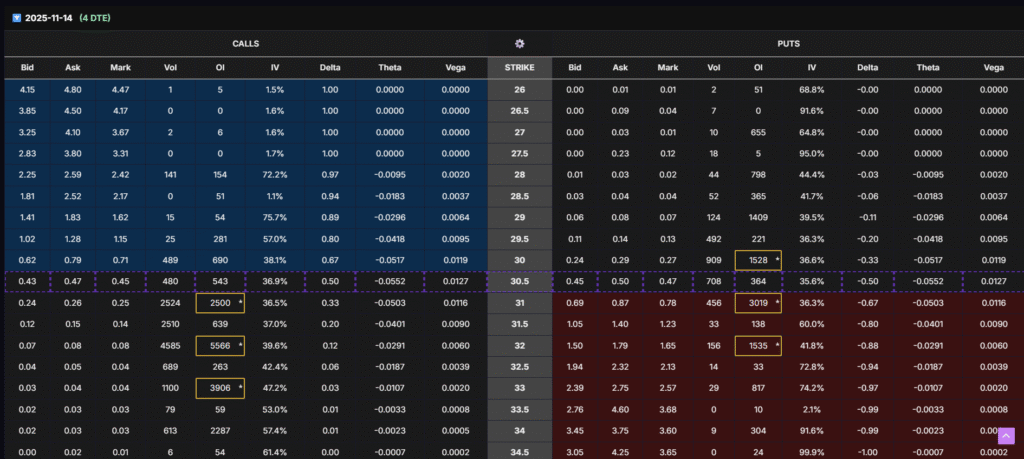

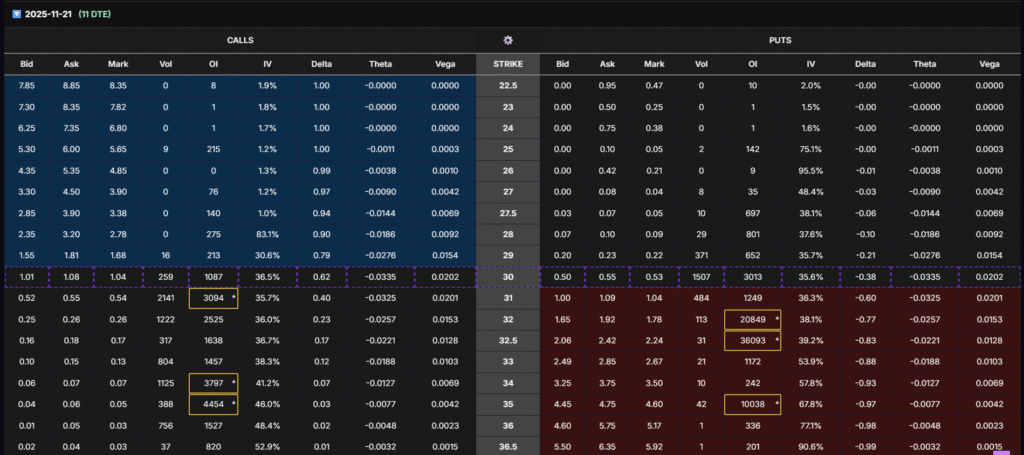

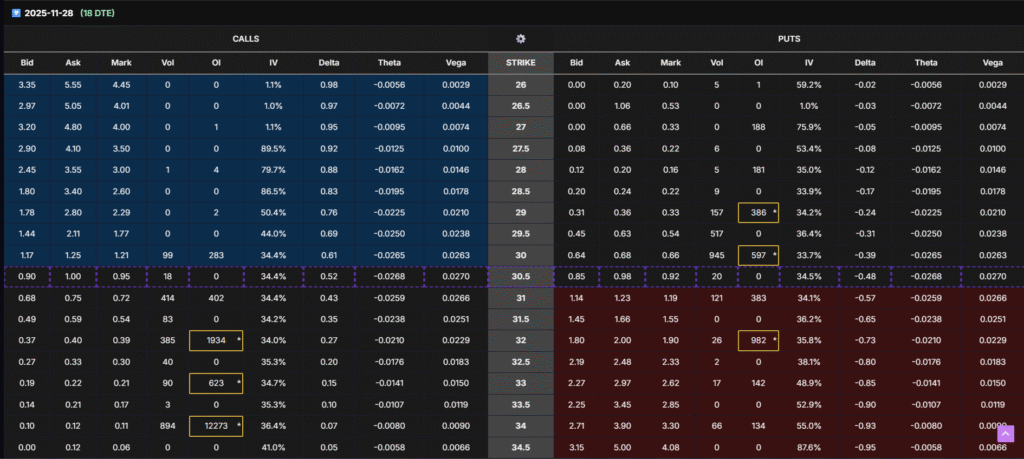

6️⃣ Options Flow Analysis

Recent short-term chains (Nov 14–Nov 28 expirations) show significant call-side open interest clustering between $30–$33, especially at the $32 strike (12,000+ OI).

- The highest short-term OI concentration sits just above current spot prices, indicating bullish speculative flow.

- Implied volatility for near-term expirations is still low (~35–40%), providing a favorable entry window for long-vega strategies.

- If CMG rises above $31.5–32, dealers will likely flip gamma-positive, potentially triggering a small-scale gamma squeeze toward $33–34.

Overall Options Flow Bias: Short-term bullish / medium-term accumulation phase.

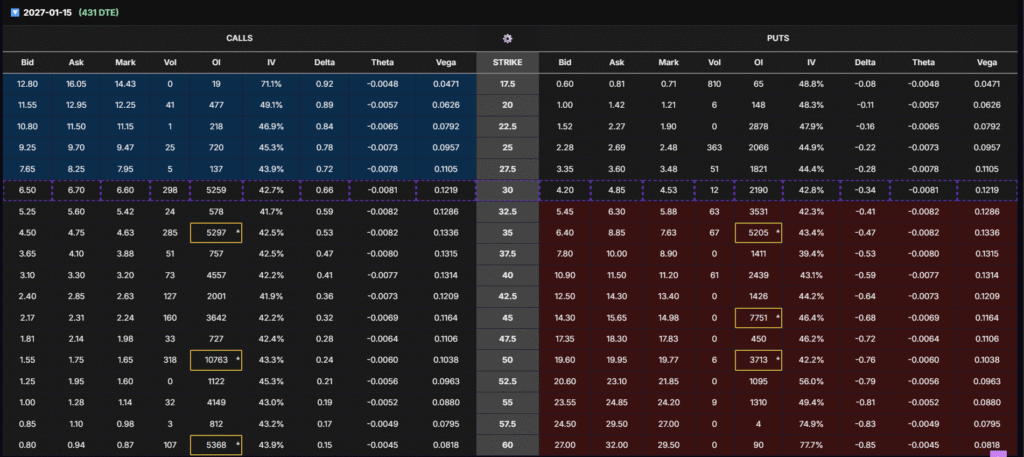

7️⃣ The LEAPS Options Setup (Core Strategy)

We are targeting the January 15, 2027 $35 strike call (≈500 DTE).

Here’s why:

| Metric | Value | Comment |

|---|---|---|

| Delta | 0.53 | Balanced exposure for moderate delta gain |

| Vega | 0.1336 | High — ideal for IV expansion profit |

| IV (Current) | 42.5% | Low relative to CMG’s historical average |

| Open Interest | 5,297 | High liquidity & tight bid-ask spreads |

This setup focuses on buying volatility cheap and selling it high before the next earnings catalyst.

- The position profits primarily from Vega expansion (rising implied volatility pre-earnings) and Delta (price recovery from oversold levels).

- We’re not betting on CMG surpassing $35; instead, we’re capturing volatility expansion.

- Once Vega spikes (typically 2–4 weeks before earnings), we aim for a +60–100% return, with the option to take partial profits at +80%.

If the options price rises +80%, traders can consider closing two-thirds of the position and leaving one-third to potentially exceed 100% gains.

8️⃣ Entry & Risk Management Plan

We will enter in 3 batches:

- Batch 1: Enter now while Vega is low and CMG trades at multi-year support.

- Batch 2: Enter in 1–2 weeks if the first batch’s option price drops -40% to -50% (of the option’s price, not the stock price).

- Batch 3: Enter in another 1–2 weeks if the second batch’s option price drops -40% to -50%.

Each batch allows dollar-cost averaging while maintaining exposure to the same 2027 $35 call strike.

Holding Duration:

Although the LEAPS have ~500 DTE, we only plan to hold for 6–8 weeks max. Beyond that, Vega decay reduces efficiency. If profits remain flat after two months, we’ll roll to a new LEAPS cycle to refresh time value.

Allocation:

Invest no more than 2% of total portfolio capital into this position. CMG remains a fundamentally solid but volatile equity, and proper position sizing is crucial.

⚠️ Disclaimer

This content is for educational and informational purposes only. Options trading involves substantial risk and is not suitable for every investor. Always perform your own due diligence or consult a licensed financial advisor before trading.

Past performance is not indicative of future results. Limit exposure to 2% of total portfolio capital per batch to ensure proper risk control.