Overview

BioCryst Pharmaceuticals (NASDAQ: BCRX) has entered a prime setup for a vega-delta hybrid LEAPS strategy, where volatility compression, institutional call buildup, and oversold technicals converge at a multi-year support zone.

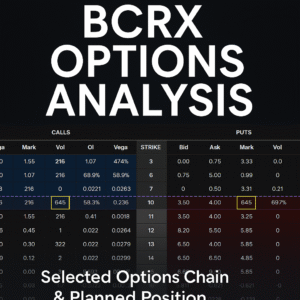

The focus of this analysis is the 2027-01-15 $10 call option (≈458 DTE) — a contract combining delta ≈ 0.4, vega ≈ 0.027, and the highest open interest (645) among long-dated strikes.

Our objective:

Buy volatility cheap and sell it high — entering before implied volatility expands ahead of BioCryst’s next major catalyst (earnings or clinical update).

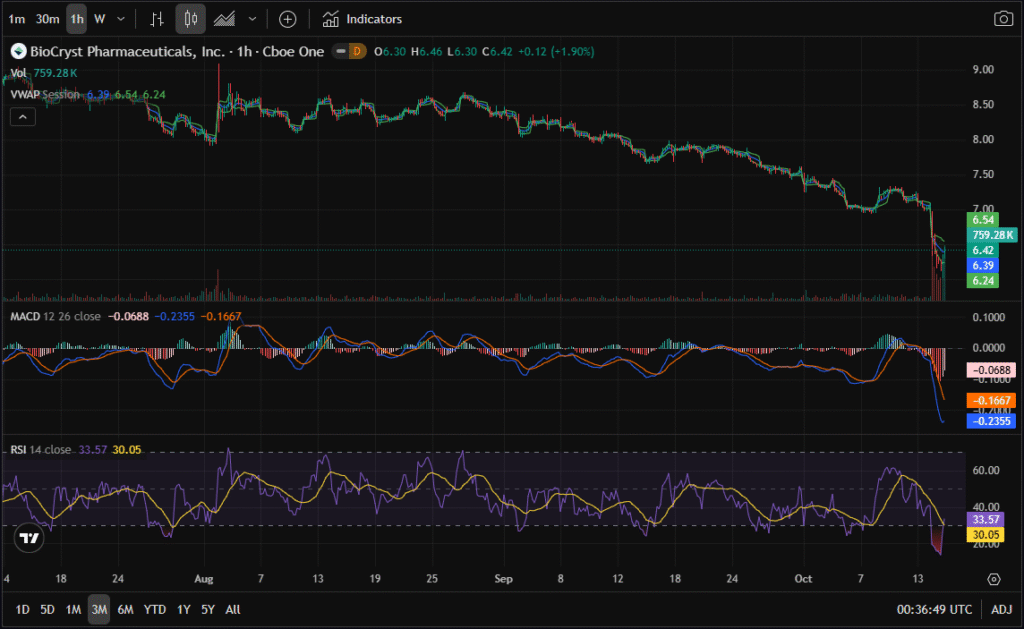

Technical Overview

Across multiple timeframes, BCRX shows a deeply oversold setup:

- 1-Year RSI: ~30 (oversold)

- MACD: Bearish momentum flattening, early signs of reversal

- Support Zone: ~$6 — historically strong multi-year base

- Volume: Spike during selloff indicates capitulation

This technical context suggests we’re likely near a volatility trough, historically followed by IV re-expansion as catalysts approach.

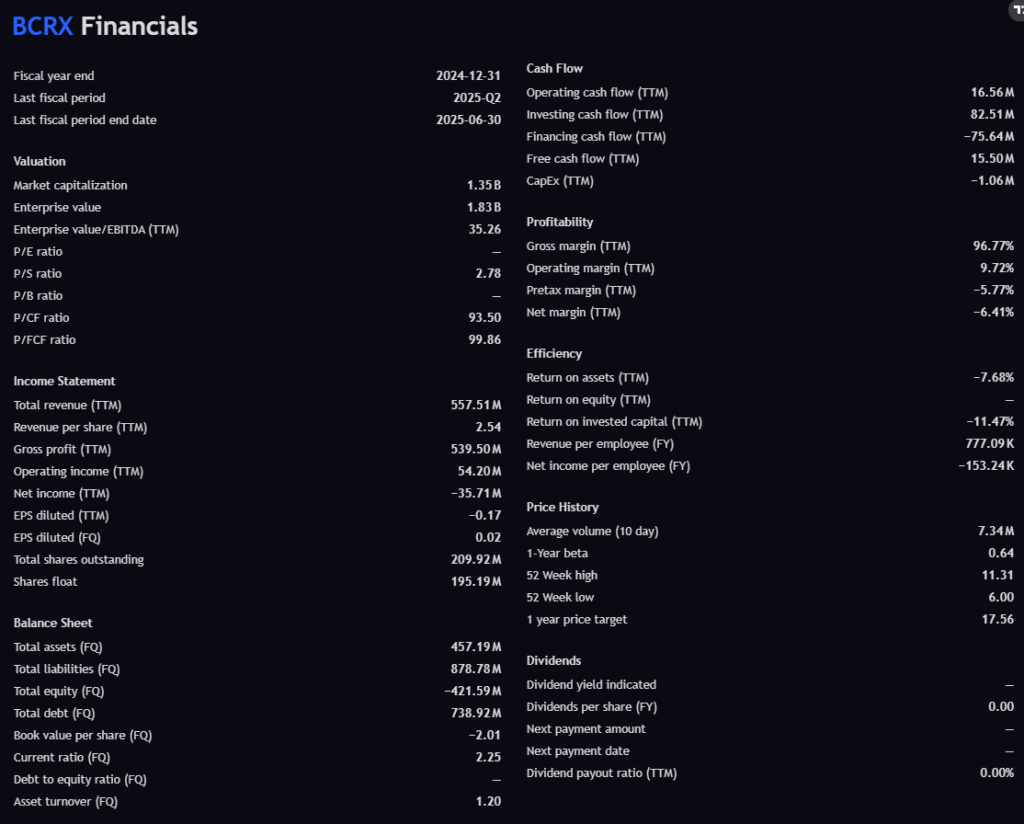

Fundamentals

BCRX’s fundamentals tell a story of strong margins but heavy leverage — typical for a small biotech entering its growth phase.

| Metric | Value | Interpretation |

|---|---|---|

| Market Cap | $1.35B | Small-cap, high sensitivity to catalysts |

| Revenue (TTM) | $557.5M | Stable growth trajectory |

| Gross Margin | 96.8% | Exceptional — strong product pricing power |

| Operating Income | $54.2M | Positive; trending upward |

| Net Income (TTM) | -$35.7M | Still in loss territory due to R&D and financing |

| Free Cash Flow (TTM) | $15.5M | Positive — rare for small biotech |

| Current Ratio | 2.25 | Healthy liquidity |

| Debt to Equity | N/A (negative equity) | Leverage risk, but manageable cash position |

🧭 Takeaway:

BioCryst generates solid cash flow and maintains high margins, giving it flexibility to pursue acquisitions like Astria Therapeutics without relying excessively on dilution. This positions it well for long-term upside once integration costs subside.

Analyst Price Targets

Recent analyst updates reveal a bullish re-rating following the Astria acquisition announcement on October 14, 2025.

| Analyst | Firm | Target | Price at Post | Sentiment |

|---|---|---|---|---|

| RBC Capital | Oct 14, 2025 | $15.00 | $6.42 | Bullish |

| Jefferies (Maury Raycroft) | Oct 14, 2025 | $15.00 | $6.42 | Bullish |

| Evercore ISI | Oct 1, 2025 | $8.00 | $7.24 | Neutral |

| Barclays (Gena Wang) | Aug 6, 2024 | $7.00 | $7.51 | Neutral |

🧠 Interpretation:

Despite the stock’s steep decline, two major upgrades (Jefferies and RBC) arrived within hours of the M&A call — both setting $15 price targets, implying over 130% upside from current levels.

This suggests institutional confidence in BioCryst’s multi-product portfolio and its ability to execute on post-acquisition growth.

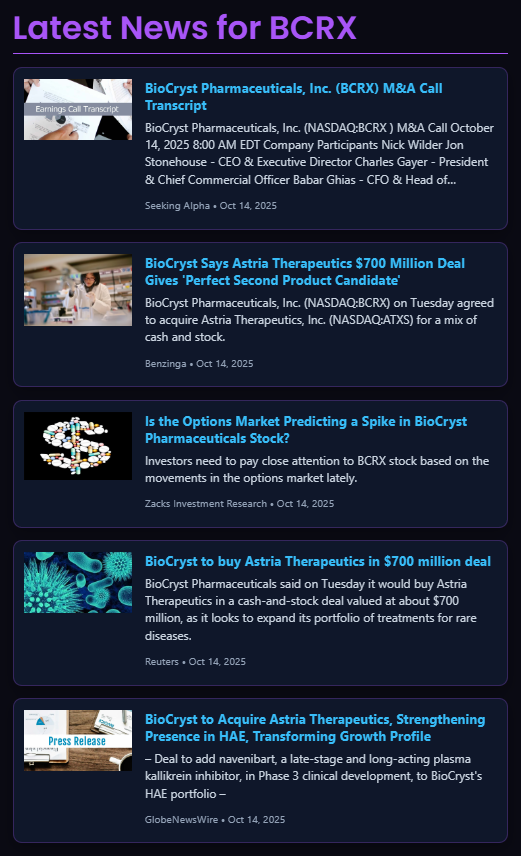

Recent News Headlines

Recent headlines provide the macro context for this setup:

- BioCryst to Acquire Astria Therapeutics in $700M Deal (Reuters, Oct 14, 2025)

→ Expands BCRX’s rare-disease pipeline, adding Astria’s naveibrant drug candidate. - BioCryst Says Astria Deal Gives “Perfect Second Product Candidate” (Benzinga, Oct 14)

→ Diversifies revenue streams beyond Orladeyo. - BioCryst M&A Call Highlights Confidence in Growth Profile (Seeking Alpha)

→ CEO and CFO reiterated synergy-driven long-term potential. - Options Market Predicts Spike in BioCryst Volatility (Zacks Research)

→ Confirms rising speculative call flow before the announcement.

🧩 Interpretation:

The headlines show strategic optimism and market repositioning following the acquisition — both precursors to volatility expansion. The deal effectively transforms BioCryst from a single-product biotech into a multi-asset rare-disease platform.

Insider & House Trading Activity

Insider Transactions

- CFO Babar Ghias: Acquired 305,000 shares (M-Exempt) at ~$8.55 — major confidence signal.

- Directors Amy McKee, Frank Steven, Vincent Milano: Multiple restricted stock awards in August.

- Director Theresa Heggie: Minor sale offset by large M-Exempt acquisitions.

➡️ Tone: Net bullish — insiders are accumulating or holding, not exiting.

House Trading Disclosures

- Congressman Josh Gottheimer has traded BCRX multiple times since 2022.

- Latest (Oct 2023): Purchase of $1,001–$15,000 worth of shares.

➡️ Tone: Political-level confidence and recurring accumulation pattern.

- Latest (Oct 2023): Purchase of $1,001–$15,000 worth of shares.

Options Flow Analysis

Across expirations, call-side open interest shows clear bullish accumulation:

- 2025-12-19: Strong OI concentration between $7–$9.

- 2026-01-16: Massive 7,965 OI at the $10 strike — institutional LEAPS interest.

- 2027-01-15: Peak OI (645) again at the $10 strike, with vega 0.0269 and delta 0.41 — ideal for our strategy.

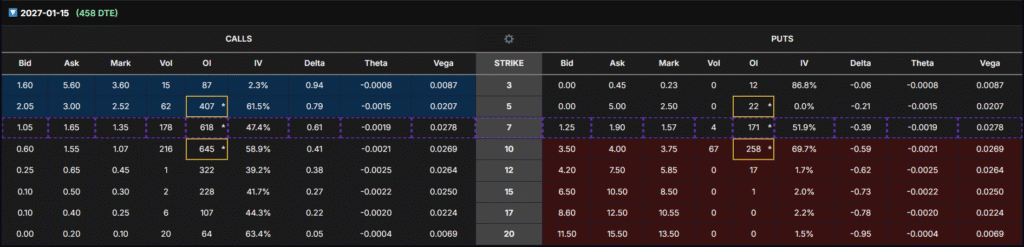

The combination of deep liquidity, balanced greeks, and cheap implied volatility (~59%) makes this contract the perfect vehicle for our vega accumulation trade.

Selected Options Chain & Planned Position

Below is the focused options chain snapshot for the January 15, 2027 (458 DTE) expiration, which we will use for this LEAPS strategy. Our emphasis is on the call side, since we are positioning to profit from vega and delta expansion rather than immediate directional movement.

| Strike | Delta | Vega | Theta | Implied Volatility (IV) | Open Interest (OI) | Interpretation |

|---|---|---|---|---|---|---|

| $7 | 0.61 | 0.0278 | –0.0019 | 47.4% | 618 | Too deep ITM — less vega impact, more expensive |

| $10 | 0.41 | 0.0269 | –0.0021 | 58.9% | 645 | ✅ Perfect balance of delta, vega, and liquidity |

| $12 | 0.38 | 0.0264 | –0.0025 | 39.2% | 322 | Slightly OTM — lower sensitivity to near-term move |

| $15 | 0.27 | 0.0250 | –0.0022 | 41.7% | 228 | Too far OTM — weaker delta and slower response |

Our Planned Position:

We are selecting the $10 Call (2027-01-15 Expiration) as our core contract for this setup.

🧭 Reasoning:

- Delta ≈ 0.4 gives an efficient 3–5× leverage on moderate price movement.

- Vega ≈ 0.027 means each 1-point increase in IV adds roughly $0.027 to the contract — a strong advantage when volatility inflates ahead of catalysts.

- Highest OI (645) ensures tight spreads and easy scaling in/out.

- Current IV ≈ 59%, historically low for BCRX — perfect for buying volatility cheap.

This makes the $10 call the optimal balance point between cost efficiency, volatility exposure, and liquidity — a setup professional funds favor for volatility-cycle trades.

Position Structure Recap

- Contract: BCRX 2027-01-15 $10 Call

- DTE: 458

- Greeks: Δ 0.41 / Θ –0.0021 / Vega 0.027

- Entry Intent: Buy when volatility is quiet, sell when it expands

- Exit Target: +80–110% profit pre-earnings or pre-catalyst

- Roll Strategy: If no move within 2 months, roll to a new long-dated contract

Strategy: Buying Vega Cheap, Selling Vega High

This setup isn’t about guessing the exact stock price; it’s about capturing volatility expansion and delta leverage.

When BCRX trades around $6.40:

- Each 1-point IV rise adds roughly $0.027 to the option price.

- A 25–35 point IV rise before earnings could increase the option’s value by +$0.68–$0.95 per contract, before any delta gains.

- If the stock moves just +10%, the option could move +40–50% from delta expansion alone.

💡 Profit window:

Expect +80–110% returns within two months before earnings, driven by vega and delta synergy.

Three-Batch Entry Plan

| Batch | Timing | Condition | Objective |

|---|---|---|---|

| Batch 1 | 🔹 Enter now | Volatility is cheap | Establish base position |

| Batch 2 | 1–2 weeks later | Options price drops –40–50% | Average down, add exposure |

| Batch 3 | 1–2 weeks after Batch 2 | Options price drops –40–50% again | Final layer before catalyst |

🔁 Key Reminder: “–40–50%” refers to the options price, not the stock price.

💰 Profit-taking: When your options price rises +80%, consider closing 2/3 of the position and let the remaining 1/3 run for potential 100%+ gains.

If the options fail to move within two months, roll forward to maintain exposure while resetting theta.

Summary

| Category | Signal |

|---|---|

| Technicals | Multi-year support, oversold RSI |

| Fundamentals | 96% margin, positive FCF |

| Analyst Consensus | $15 PT (130% upside) |

| News Flow | M&A growth catalyst, bullish tone |

| Insider Sentiment | Accumulation & confidence |

| Options Structure | $10 LEAPS call (delta 0.4, vega 0.027, OI 645) |

| Strategy | Buy low IV → sell high IV before earnings |

| Target | +80–110% pre-catalyst profit window |

⚠️ Disclaimer

This article is for informational and educational purposes only and not financial advice. Options trading involves significant risk and may not be suitable for all investors. Always use proper position sizing and stop-loss discipline.

Allocate no more than 2% of total portfolio capital per batch (total 6% across all three).

If the options price falls –40–50%, use that as a planned entry point for the next batch.

If the options price rises +80%, consider closing 2/3 of your position to lock in profits while keeping 1/3 open for potential upside beyond 100%.

Holding period should not exceed 2 months. If the position remains flat, roll forward to a fresh expiration with similar delta/vega exposure.