Thesis

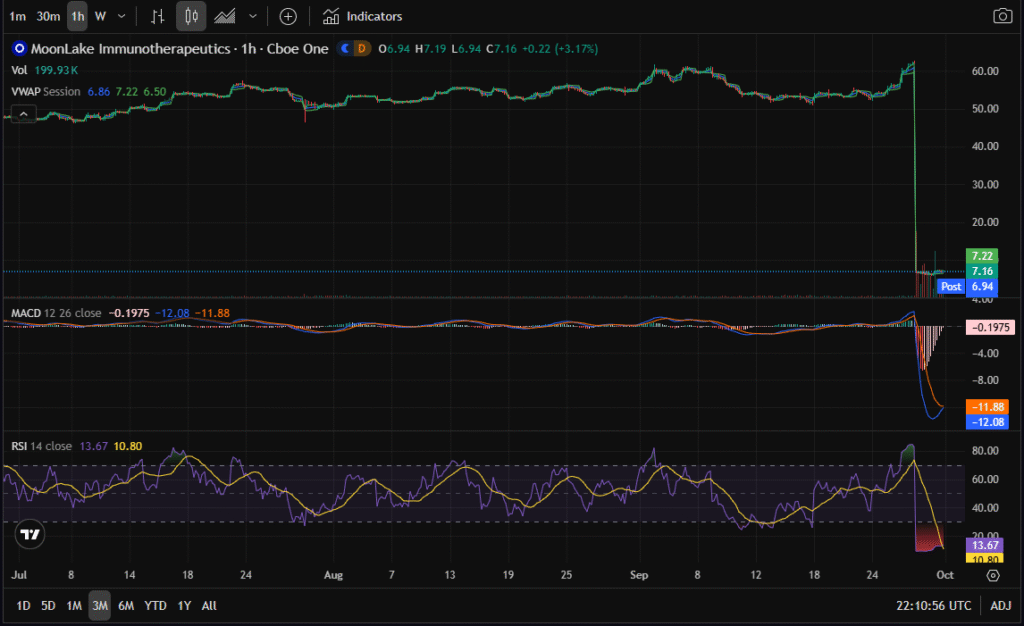

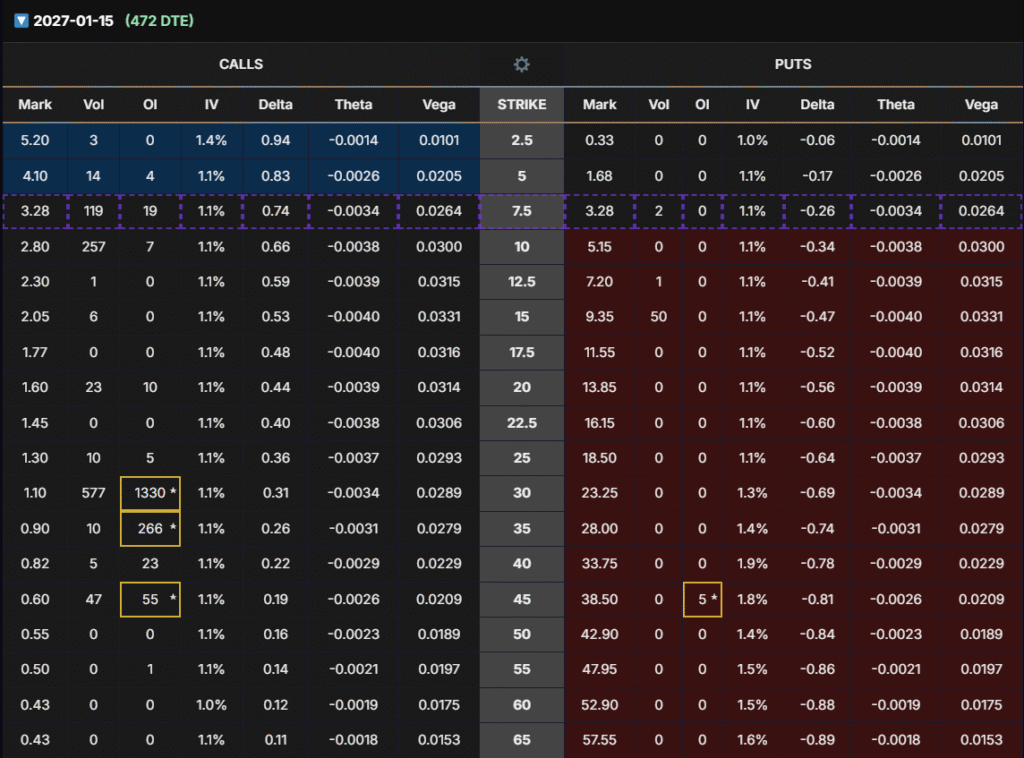

MoonLake Immunotherapeutics (MLTX) cratered ~90% after Phase 3 VELA-2 disappointment and is now trading near all-time/52-week lows. The panic flush reset options pricing: Vega is cheap; Delta is reset. Our plan is to buy long-dated calls now and harvest the pre-catalyst IV ramp, closing before earnings or major updates. Core contract: ~500 DTE $10C (Δ≈0.60, high OI/liquidity, strong Vega).

Targets/Rules

- Profit target: +80% (base), stretch: +100–110%

- Max hold: 2 months → if not working, roll, don’t hold and bleed

- Risk: Allocate ≤2% of portfolio to this idea

What the Charts Say (context for the options trade)

- Momentum washout: RSI plunged to extremely oversold on 3M/1Y/All-time; MACD shows heavy bearish cross but short-term histogram flattening (typical into a reflex bounce).

- Structural damage: All key supports snapped; any rally is a repair bounce, not an instant trend reversal.

- Setup relevance: Post-crash regimes often see implied volatility rebuild over the 2–6 weeks ahead of earnings/updates—exactly the edge we’re aiming to monetize.

News Catalyst Wrap (why the reset happened)

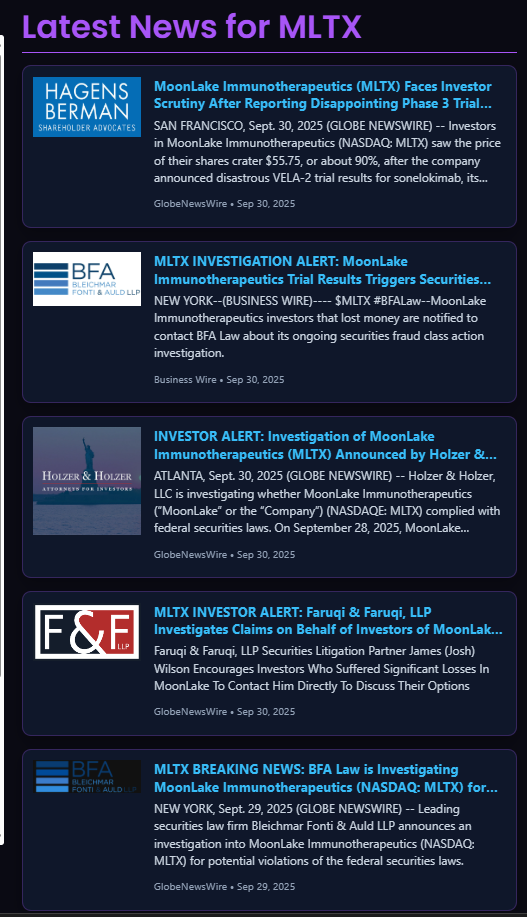

- Catalyst: Company reported disappointing Phase 3 results (VELA-2, sonelokimab) → institutional de-risking and gap-down collapse.

- Aftermath: Multiple firms (e.g., Hagens Berman, Holzer & Holzer, Faruqi & Faruqi, BFA Law) announced shareholder/class-action investigations, adding headline pressure.

- What it means for options: After the event shock, IV/vega were crushed; historically, IV rebuilds into the next scheduled update. We’re positioning to buy IV low and sell IV high ahead of that date.

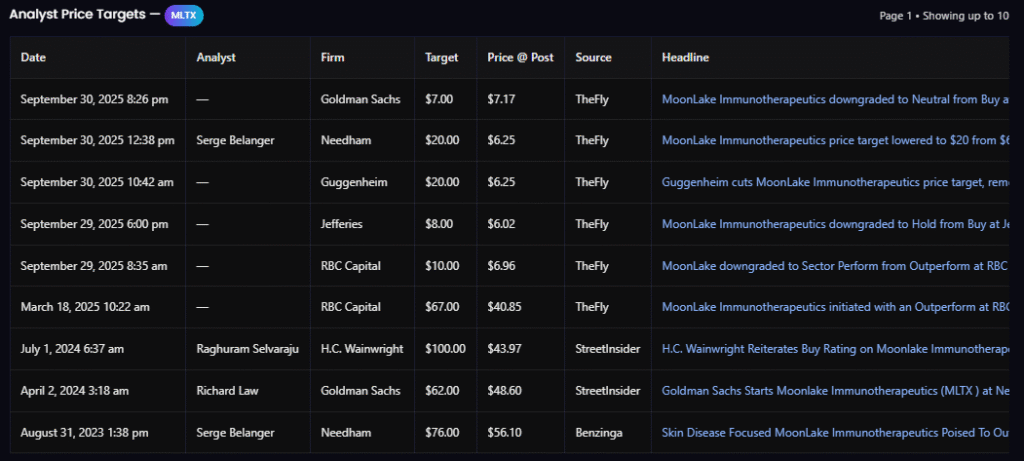

Analyst Price Targets (street reset)

- Post-crash cuts:

- Needham → $20

- Guggenheim → $20

- RBC → $10 (Sector Perform)

- Jefferies → $8 (Hold)

- Pre-crash context: PTs in $62–$100 range (GS/Wainwright/Needham/RBC) are now obsolete.

Read: Street now implies a single-digits to low-teens trading band near term, with a recovery optionality case (upper bound $20) if the pipeline narrative stabilizes.

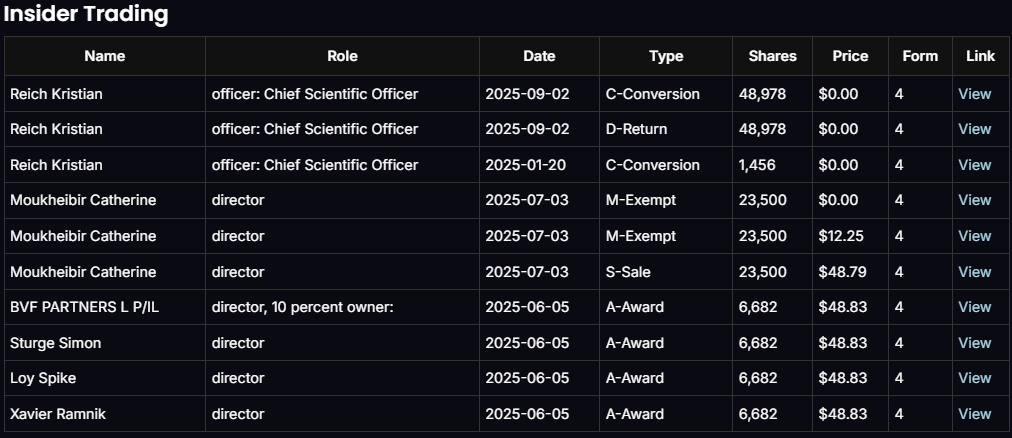

Insider Trading Read-Through

- Director sale: One director sold ~23,500 shares @ ~$48.79 (pre-collapse) — optics are poor and will be cited in suits.

- CSO/admin moves: Conversions/returns showed administrative activity, not open-market buys.

- No “buy-the-dip” by insiders post-crash → no visible insider confidence yet. This reinforces that any near-term upside is more technical/IV-driven than fundamental.

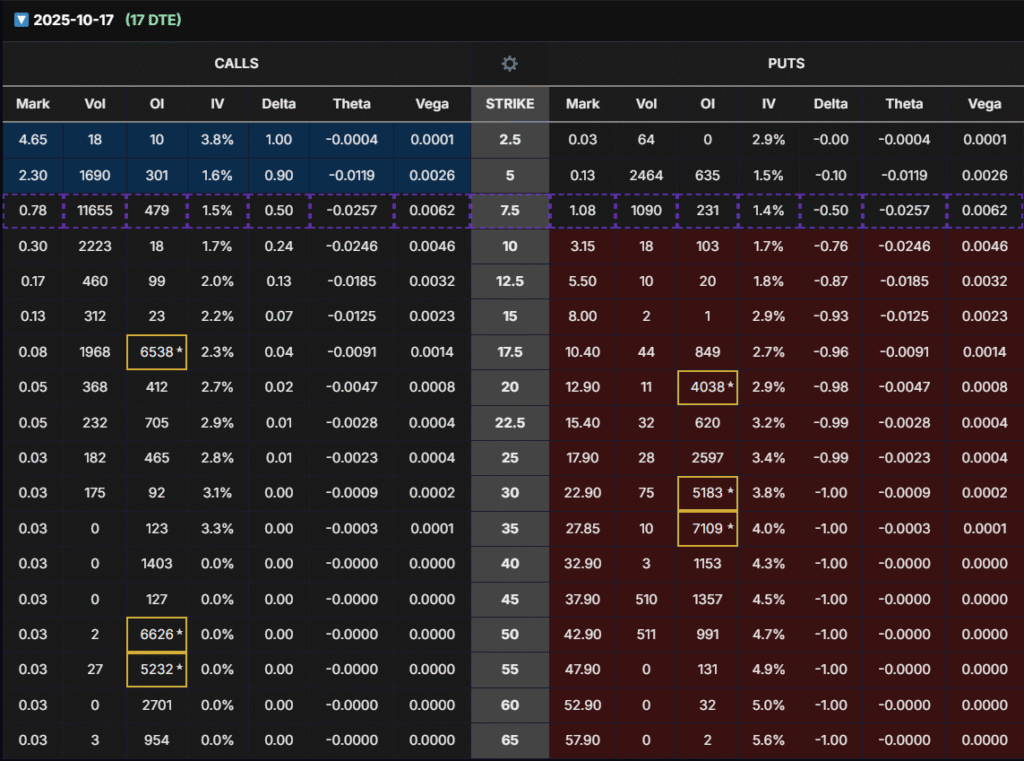

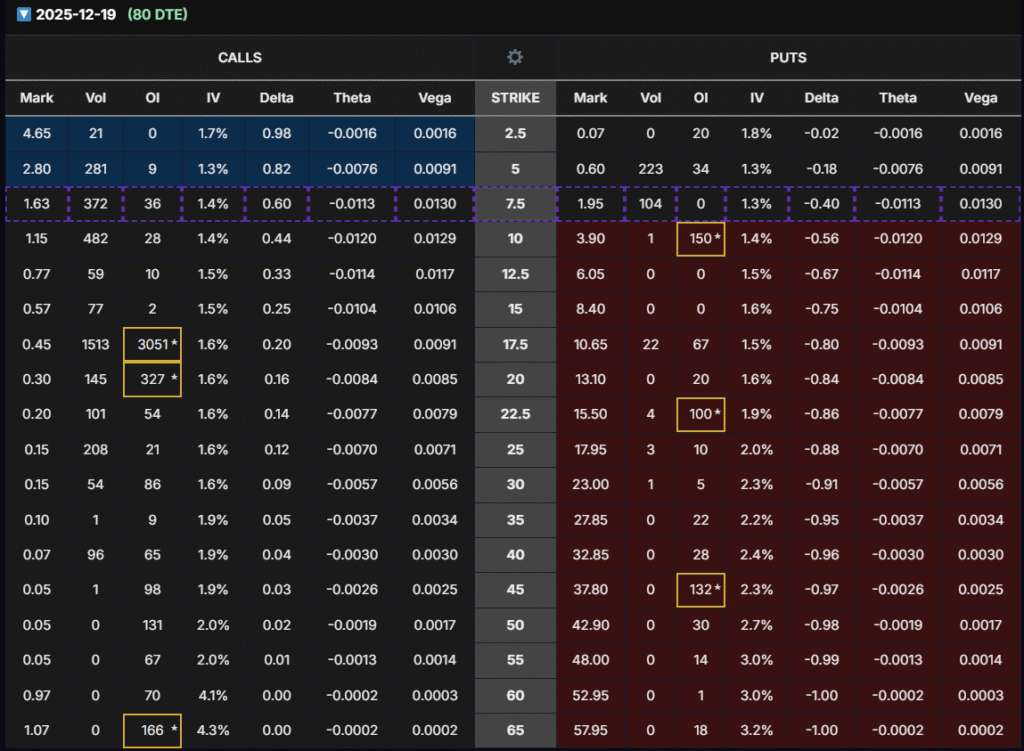

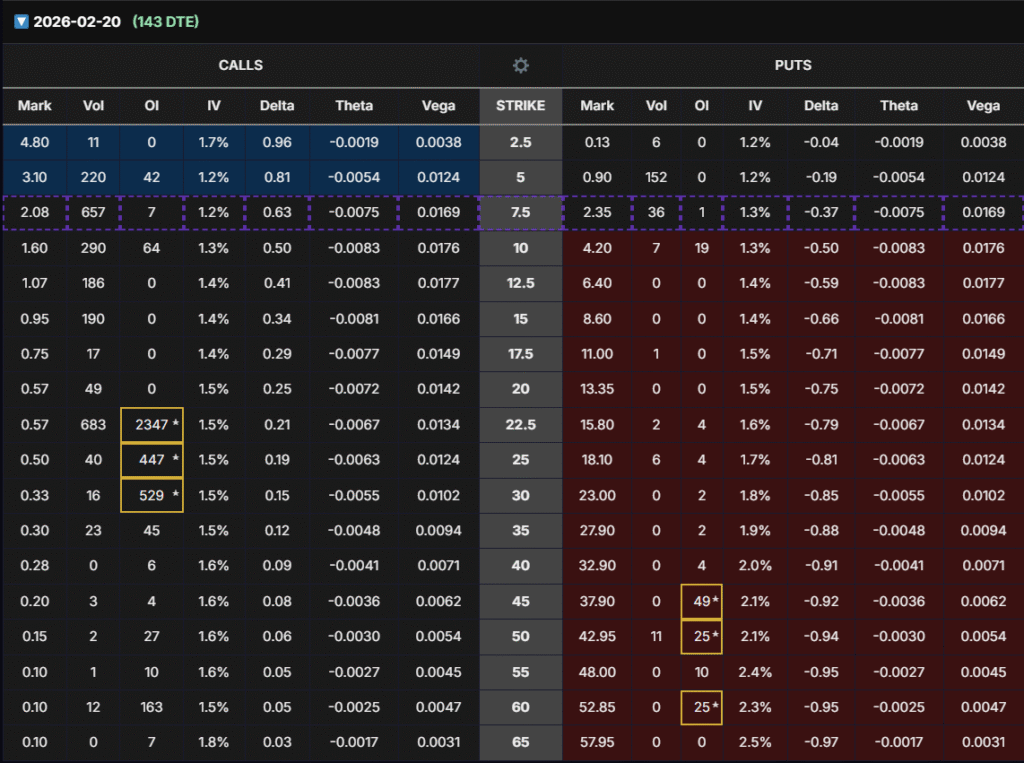

Options Flow (Calls) — is positioning bullish or bearish?

Oct 17, 2025 (17 DTE):

- Big OI $7.5C (~11,655) and $10C (~6,538) → speculative bounce positioning close to spot.

Dec 19, 2025 (80 DTE): - Largest cluster $12.5C (~3,051) → market eyeing a stabilization toward low teens.

Feb 20, 2026 (143 DTE): - Notable OI at $22.5C (~2,347) plus $25–30C tails → lottery-ticket recovery bets.

Verdict: Call-side OI clusters skew bullish/hopeful (short-term bounce + longer-dated upside speculation). It’s not classic institutional conviction—more tactical/speculative—but it supports our pre-catalyst IV/Delta plan.

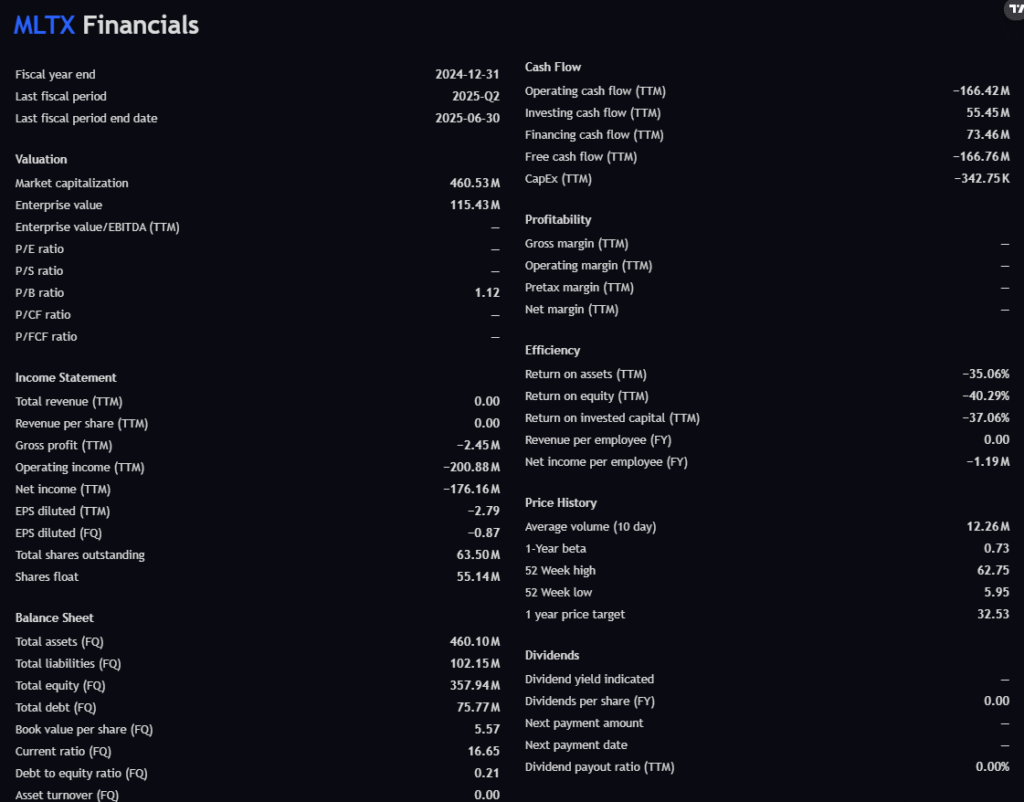

Financial Snapshot (risk lens)

- Revenue TTM: $0 (clinical-stage)

- FCF TTM: –$166.8M (heavy burn)

- Current Ratio: ~16.7 (ample near-term liquidity)

- Debt/Equity: ~0.21 (low leverage)

Read: Balance sheet buys time, but dilution risk remains if pipeline progress stalls. This is precisely why we trade the pre-catalyst IV rather than invest for a distant commercialization.

The Trade — LEAPS to Buy Vega Low, Sell Vega High

Contract: ~500 DTE $10 Call (Δ≈0.60, high OI/liquidity, higher Vega than deep-ITM)

Why $10C?

- Δ≈0.60 provides 3–5× sensitivity to stock moves

- Vega meaningfully higher vs. deeper ITM → best to monetize IV ramp

- One of the highest liquidity strikes on the LEAPS board

What we’re monetizing:

- IV/Vega expansion into earnings/pipeline update, and

- Δ-assisted bounce from a historically oversold state.

Exit: BEFORE earnings (avoid IV crush). Targets: +80% base, +100–110% stretch.

3-Batch Scaling Plan (very important)

- Batch 1 — Enter Now: Buy the ~500 DTE $10C.

- Batch 2 — Add Later: If the options price of Batch 1 pulls back –40–50% (of the options price) within 1–2 weeks, add the second batch.

- Batch 3 — Add Later: If the options price of Batch 2 falls another –40–50% (of the options price) in the following 1–2 weeks, add the third batch.

Note: The –40–50% triggers refer strictly to the options price, not the stock price.

Max Hold: 2 months. If we’re not near targets or IV hasn’t expanded, roll (same strike/next cycle or adjust strike to re-center Δ≈0.55–0.65).

Monitoring Checklist

- IV trend: IV percentile rising? (should advance 2–4 weeks pre-event)

- Price momentum: RSI back >30; MACD crossover on daily

- Flow: Does call-side OI migrate higher (e.g., $10 → $12.5)?

- Liquidity: Spreads tight enough (≤5–10% of premium) for exits

- Calendar: Confirm earnings/updates window and exit ahead of it

Final Word

MLTX is a binary biotech whose equity just reset. That’s exactly the regime where pre-catalyst volatility trades can shine. The ~500 DTE $10C gives us the best mix of vega + delta + liquidity to exploit the IV rebuild, with a disciplined 3-batch plan, tight risk, and a hard no-earnings-hold rule.

⚠️ Risk Disclosure / Allocation Guardrails

This content is for educational purposes only and not financial advice. Options are risky and can lose 100% of the premium. Limit exposure to no more than 2% of total portfolio per this speculative idea, use only risk capital, and follow the plan to close prior to the catalyst to avoid IV crush.