This is a reanalysis of Keurig Dr Pepper (NASDAQ: KDP), following up on our earlier options strategy. In our first review, we entered the initial batch of LEAPS calls to position ahead of implied volatility expansion. Now, with option pricing lower and earnings approaching in one month, we are entering our second batch. This setup combines technical oversold conditions, fundamental resilience, and a powerful options flow skew that favors a pre-earnings rebound.

📊 Technical Overview

- 3M Chart: KDP collapsed from $36 to ~$26, RSI extremely oversold, MACD bearish but flattening.

- 1Y Chart: At 1-year lows, RSI ~20, potential bullish MACD crossover emerging.

- 5Y Chart: Stock testing levels last seen during COVID-19 lows, RSI oversold, and historically a zone where rebounds occur.

📉 Fundamentals

- Strengths: $1.6B free cash flow, strong gross margin (~52%), manageable debt-to-equity (0.71).

- Weaknesses: Net margin (~9.7%) below KO/PEP, high payout ratio (~82%), weak ROE (6.2%) and ROIC (3.9%).

- Dividend: 3.3% yield provides stability but growth is limited.

Insider trades have been administrative (grants/exemptions), not conviction buys. Senate/House political trades lean bearish, suggesting broader caution.

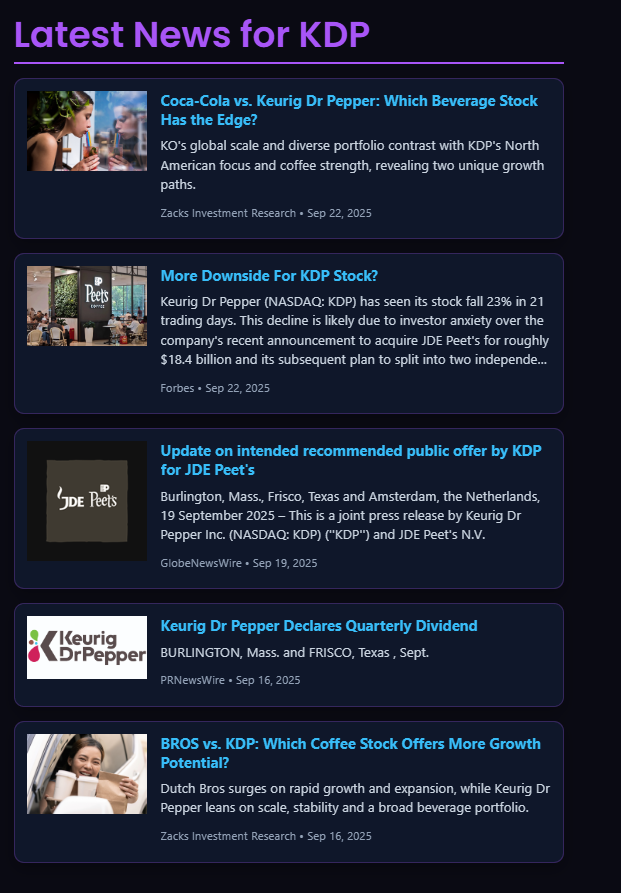

📰 News Headlines – Market Sentiment

- Coca-Cola vs. KDP Comparisons: Analysts stress KO’s global moat versus KDP’s North America focus → sentiment negative.

- “More Downside for KDP?” (Forbes): Warning of pressure from $18.4B JDE Peet’s acquisition + spin-off uncertainty.

- Official JDE Peet’s Deal Press Release: Validates the acquisition but spooked markets over leverage.

- Dividend Declaration: Confirms financial stability, though payout stretched.

- BROS vs. KDP (Zacks): Positions KDP as a defensive income stock, not a growth play.

👉 Sentiment Impact: Headlines reinforce near-term bearishness but also highlight KDP’s defensive cash flow strength. The stock’s steep selloff is largely news-driven (M&A risk) rather than a collapse in core fundamentals.

🎯 Analyst Price Targets

Recent analyst activity shows a clear shift in tone:

- BNP Paribas: Underperform, PT $24 → Bearish floor, signals risk of further downside.

- HSBC: Downgrade to Hold, PT $30 → cautious, in line with current trading range.

- Jefferies: Buy, PT $41 → sees JDE Peet’s as a “good deal,” more optimistic.

- Barclays: $39–41 → prior bullish stance, before selloff.

- Consensus Range: $30–36 (ex-BNP) → implies 10–30% rebound potential if the market stabilizes.

👉 Takeaway: Analysts are divided — with one very bearish ($24 PT) but most clustered higher, implying the stock is oversold relative to consensus.

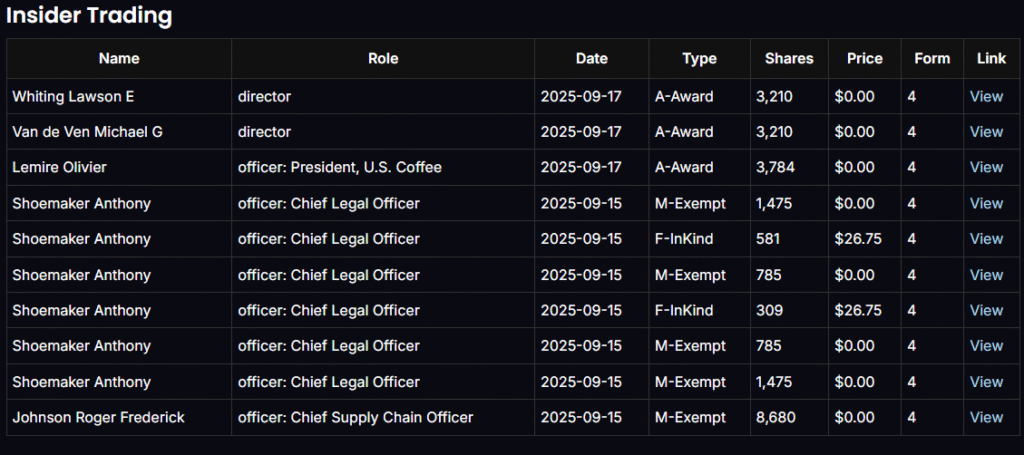

🕵️♂️ Insider & Political Trading (Pillar 6: Insider/Institutional Accumulation)

What happened (latest window):

- Insiders (Sept 15–17, 2025):

- Directors Whiting Lawson E and Van de Ven Michael G received A-Award stock grants.

- Olivier Lemire (President, U.S. Coffee) received an A-Award grant.

- Anthony Shoemaker (Chief Legal Officer) filed multiple M-Exempt and F-InKind transactions (some tax/withholding entries around ~$26.75).

- Roger Frederick Johnson (Chief Supply Chain Officer) reported M-Exempt activity.

- Signal: These are administrative/compensation filings (not open-market buying). No insider open-market purchases (code “P”) were reported in this cluster.

- U.S. Senate disclosures:

- Richard Blumenthal reported multiple sales in 2022–2023 (six-figure ranges).

- John Hoeven showed small purchases in 2019 (historical; low relevance now).

- Signal: Skews bearish/neutral; no recent Senate accumulation.

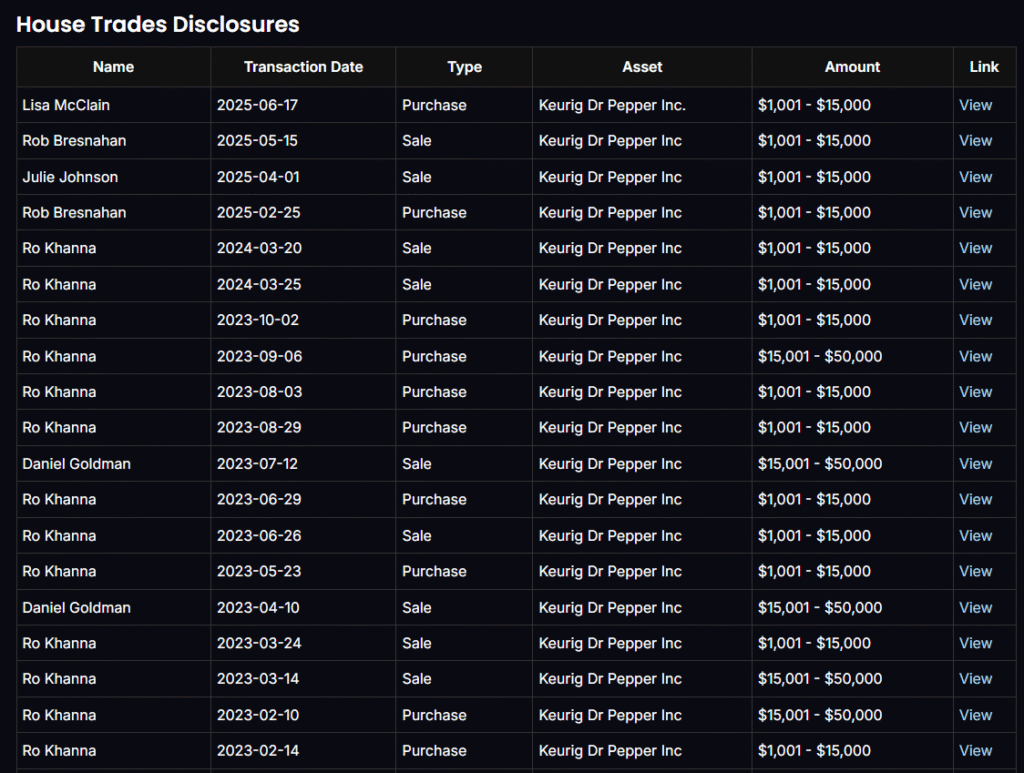

- U.S. House disclosures (2023–2025):

- Lisa McClain (Jun 2025) purchase ($1k–$15k).

- Rob Bresnahan bought (Feb 2025) then sold (May 2025) small blocks.

- Julie Johnson (Apr 2025) sale ($1k–$15k).

- Ro Khanna showed frequent small buys/sells across 2023–2024 ($1k–$50k).

- Daniel Goldman (2023) sales ($15k–$50k).

- Signal: Mixed but tilting cautious, and small-dollar—more trading than conviction.

How to read the codes:

- A-Award = equity granted as compensation (not a buy).

- M-Exempt = option/award exercise or administrative transfer (non-open market).

- F-InKind = shares withheld/returned for taxes (not a buy).

- P = open-market purchase (strongest bullish signal) — none seen in the recent filings you shared.

Bottom line:

- Current insider activity = neutral to slightly bearish (no open-market insider buys despite the big drawdown).

- Political trading = no recent large accumulation; past Senate sales and small House trades suggest caution, not conviction.

What would flip this pillar bullish:

- 2–3 open-market purchases (code “P”) by C-suite/Directors within 30–60 days.

- Cluster buys totaling $250k+ at or below current prices.

- Institutional ownership rising over the next two quarters (confirm via 13F flow).

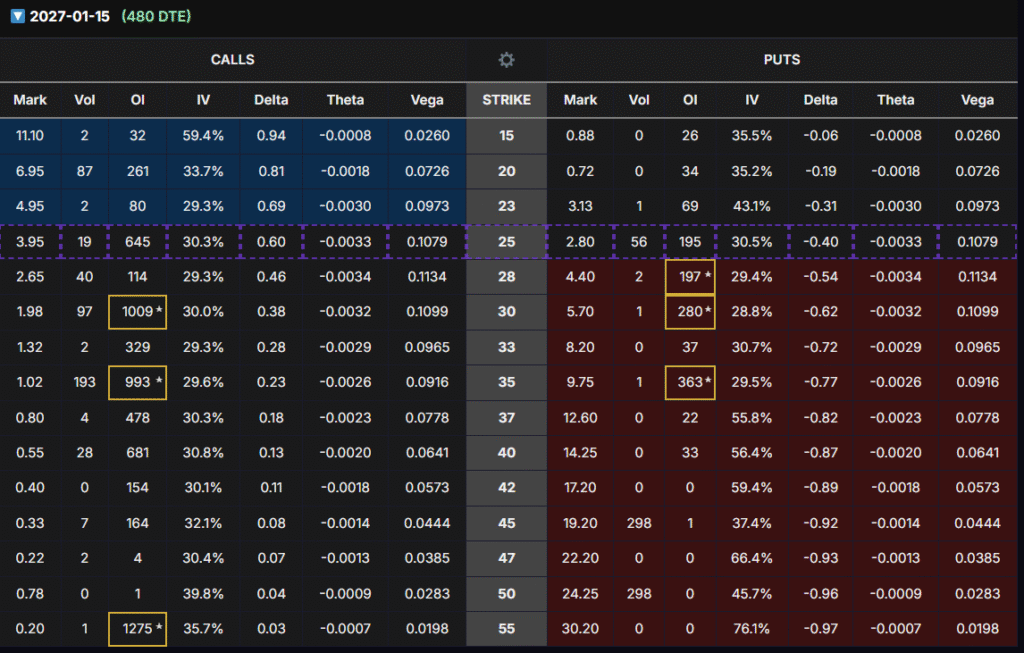

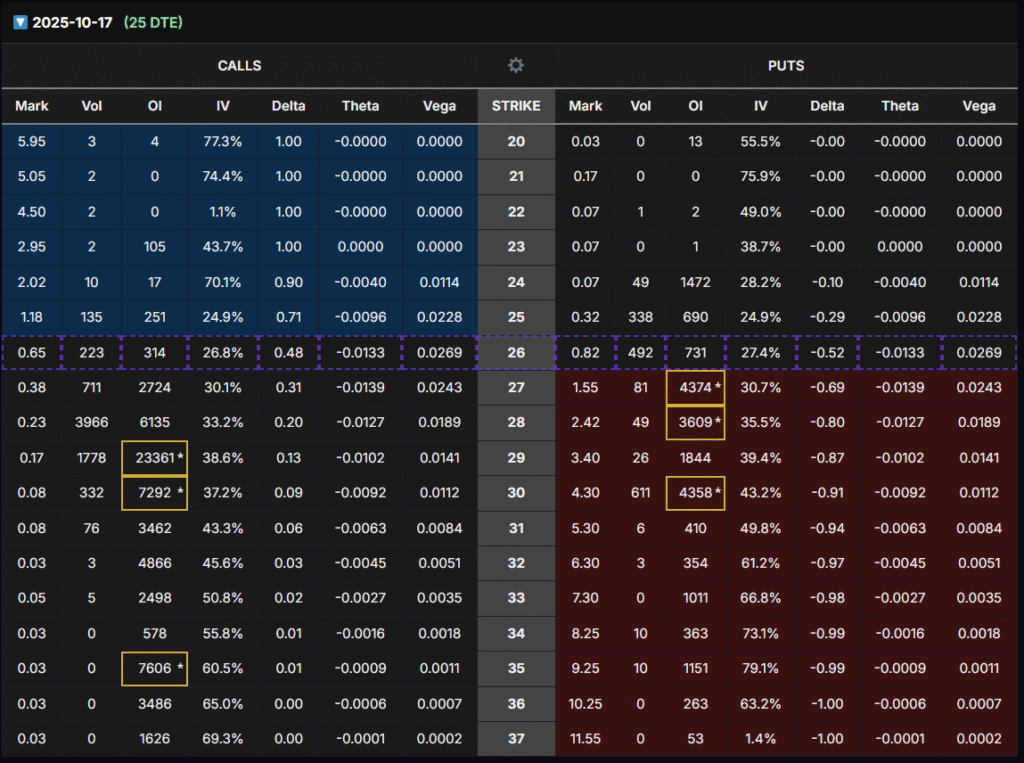

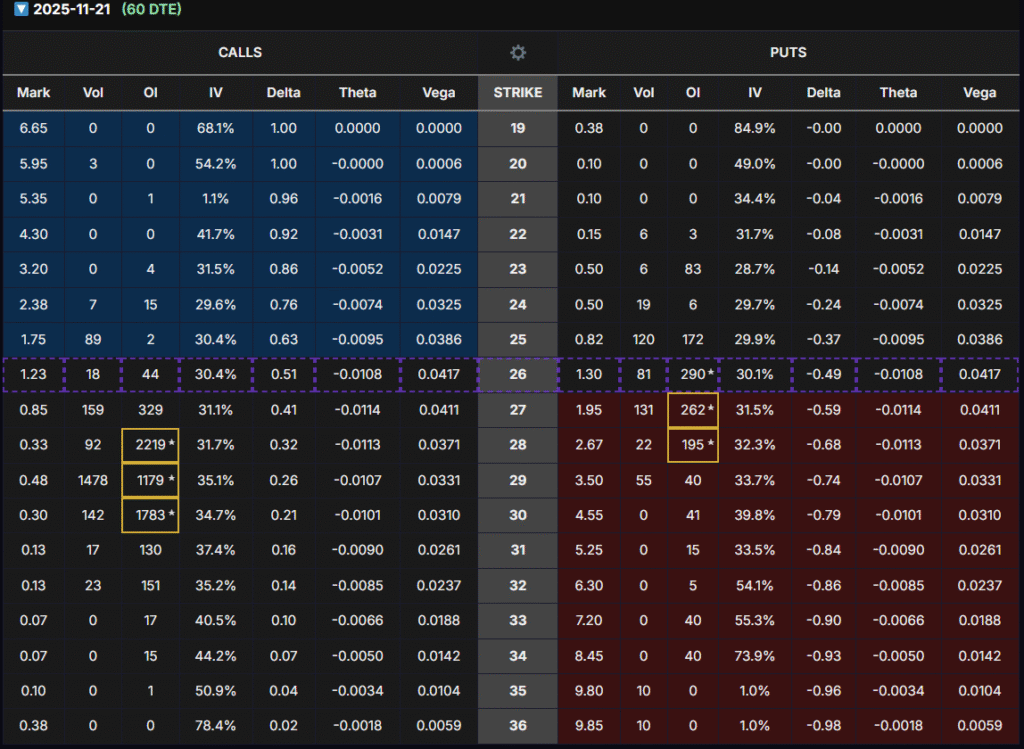

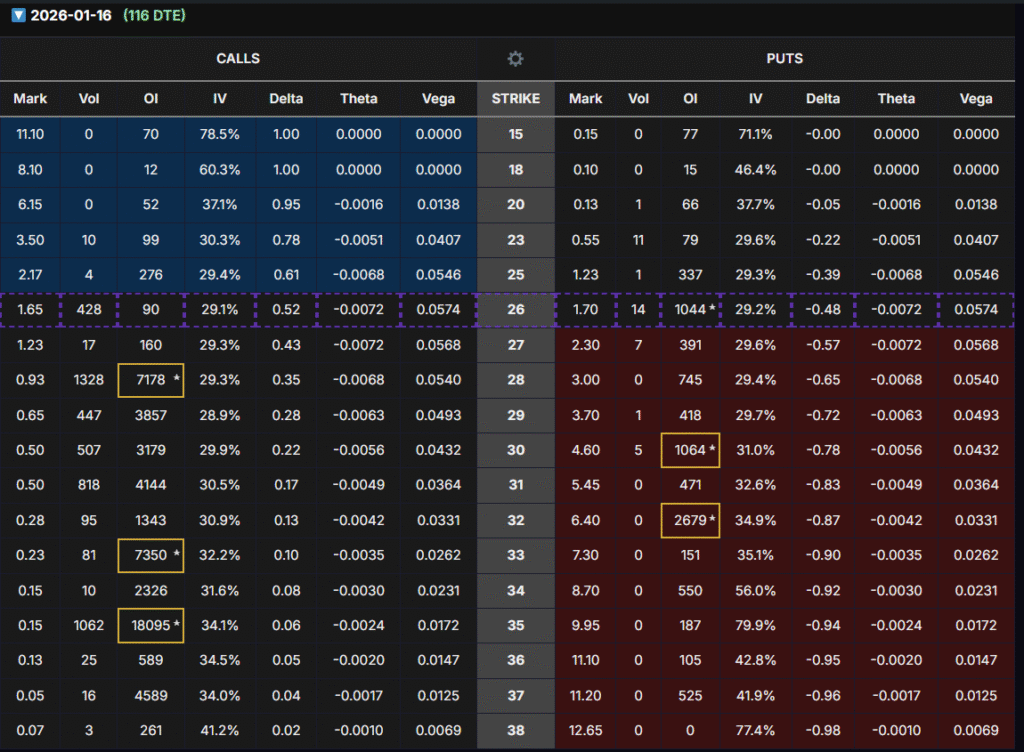

🔎 Options Chain (480 DTE – Jan 2027)

We screened for OTM strikes with Delta ~0.4, strong Vega, and liquidity. Best choice:

- KDP Jan 2027 $30 Call

- Delta: ~0.32

- OI: 993

- Vega: 0.0965

- IV: ~29%

📊 Options Flow Analysis

- 25 DTE: Heavy OI at $28C/$29C → near-term bounce bets.

- 60 DTE: $28C–$30C concentration → steady positioning.

- 116 DTE: Large OI at $28C, $30C, $34C → layering for medium-term upside.

- 480 DTE: OI heavy at $28C (~1,009), $30C (~993), $35C (~993). Longer-term speculative bullish flows visible.

👉 Flow Bias: Bullish — traders are preparing for recovery plays, with $30C positioned as the liquidity + Vega sweet spot.

🎯 Why Enter the Second Batch Now

This reanalysis highlights that option premiums are now cheaper, vega/delta compressed, and earnings are just one month away. Implied volatility is expected to ramp into earnings, creating a window for significant profit.

- Batch 1: Entered previously.

- Batch 2 (Now): Enter while options are cheaper and IV is low.

- Catalyst: IV expansion into earnings drives vega gains + delta amplification.

📌 Batch Entry Plan

- Batch 1: Already entered in prior analysis.

- Batch 2 (Now): Entry point as vega/delta are compressed.

- Batch 3 (1–2 Weeks Later): Enter if the options price of Batch 2 drops -40% to -50% (not the stock price).

📊 Expected Outcomes

- Bullish Case: Stock +10% into earnings → option value up 2–4x.

- Neutral Case: Stock flat → IV still lifts premiums to +80% profit.

- Bearish Case: Stock lower, IV cushions downside → losses manageable, next batch scales cost basis.

⚠️ Disclaimer & Risk Management

This analysis is for educational purposes only and not financial advice. Options trading is highly risky.

- Allocate no more than 2% of portfolio.

- Exit before earnings to avoid IV crush.

- Maximum hold = 2 months; roll forward if profit target not met.

- Batch entries:

- Batch 1 (entered previously)

- Batch 2 (enter now)

- Batch 3 (only if options price drops -40% to -50% from Batch 2).

✅ Final Takeaway:

This reanalysis confirms the second batch entry into KDP’s Jan 2027 $30 Calls. With cheap premiums, bullish options flow, and IV set to rise into earnings, the strategy targets 80–110% gains. By scaling in across batches and exiting before earnings, we maximize profit potential while controlling risk.