🔎 Technical Overview

Looking at the 3-month chart, FSK is trading at a recent 3-month low. The MACD has made a bullish crossover, suggesting short-term momentum is shifting away from sellers. RSI recently dipped into oversold levels and is now curling upward, pointing to the possibility of a short-term bounce.

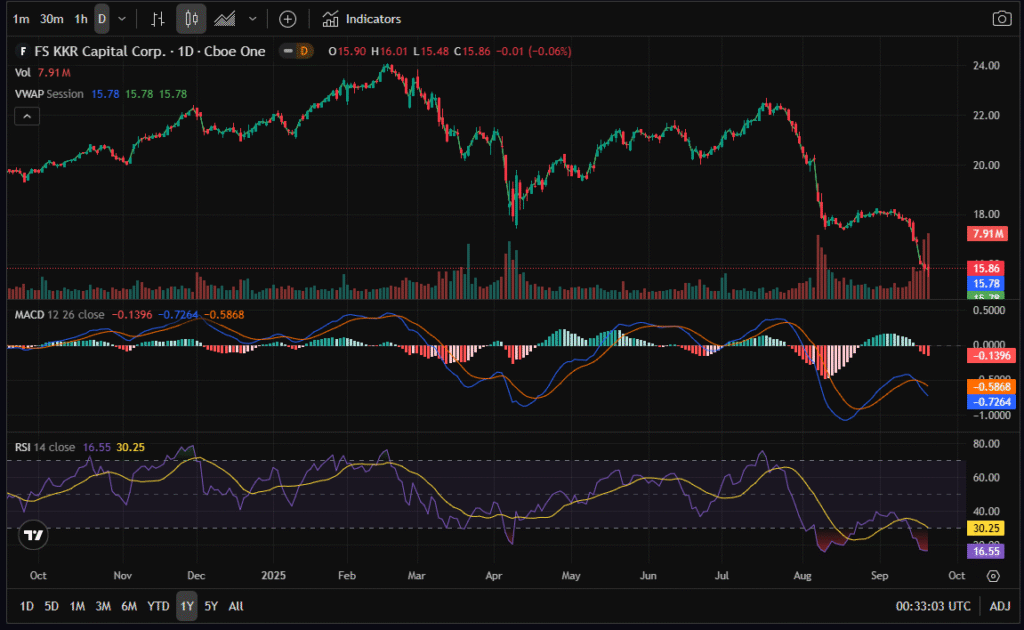

The 1-year chart shows FSK at a 1-year low, with a bearish MACD crossover still in effect and RSI deeply oversold (~16). This indicates the stock is stretched to the downside, but in a confirmed bearish medium-term trend.

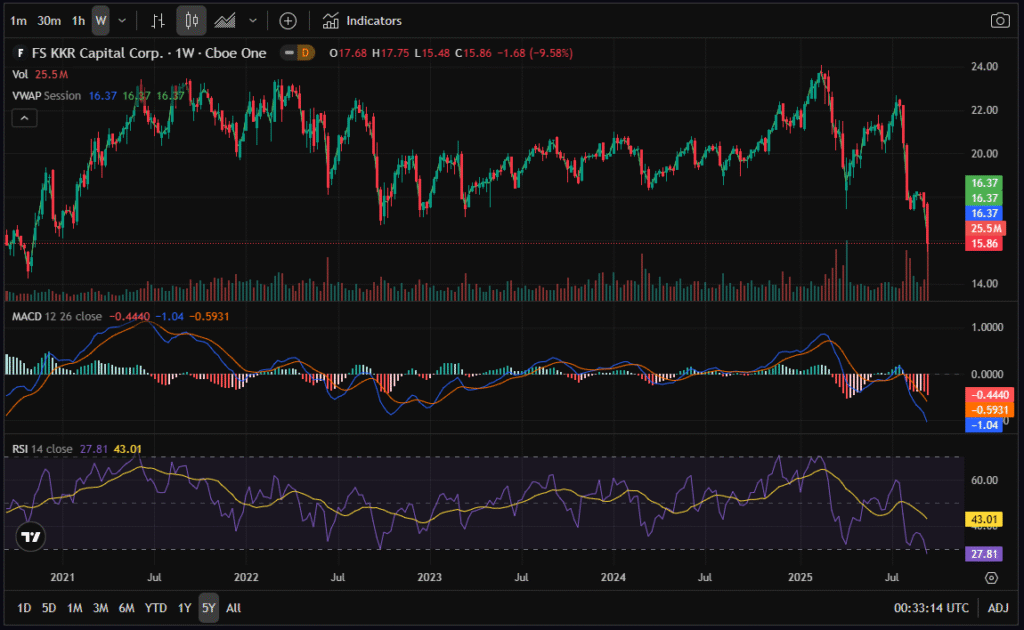

On the 5-year chart, FSK is trading close to its 5-year lows. RSI again shows oversold conditions, while MACD is bearish. Historically, RSI levels this low have preceded rebounds, but the long-term picture remains fragile.

📑 Financial Overview

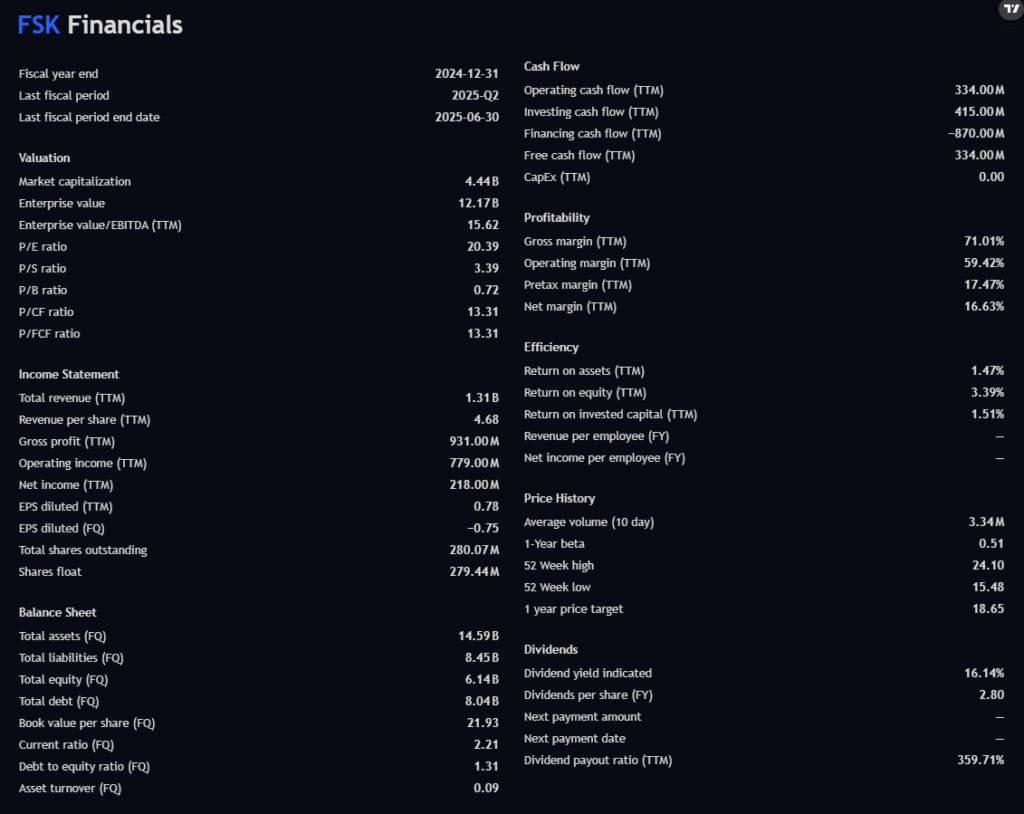

Fundamentals are mixed:

- Positive Free Cash Flow: $334M TTM, which is a strength.

- Strong Gross Margin: 71% with a healthy Net Margin of 16.6%.

- Leverage: Debt-to-equity ratio is high at 1.31, which is typical for BDCs but still a risk.

- Dividend Yield: A massive 16.14%, but the payout ratio (359%) suggests this is not sustainable long-term.

- Valuation: Trades below book value (P/B 0.72), making the stock look undervalued on an asset basis.

🏦 Analyst Price Targets

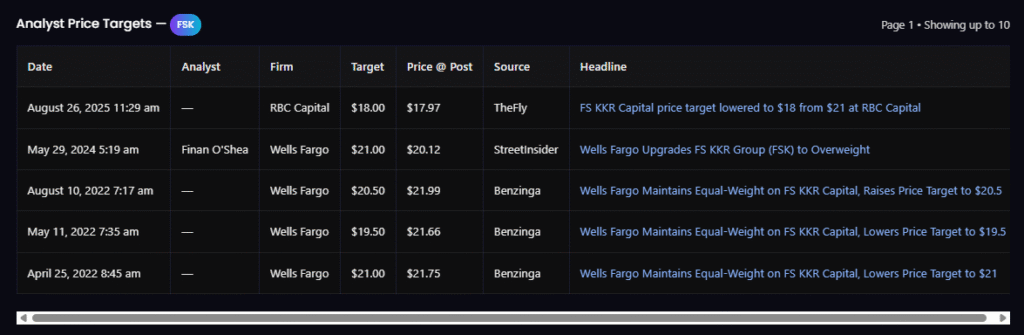

- RBC Capital (Aug 2025): Target $18.00 (cut from $21).

- Wells Fargo (May 2024): Target $21.00, upgraded to Overweight.

- Historical targets have trended downward from $21–20.5 → $18 today.

This indicates modest upside (about 13–15% from current levels), but analysts are cautious on growth prospects.

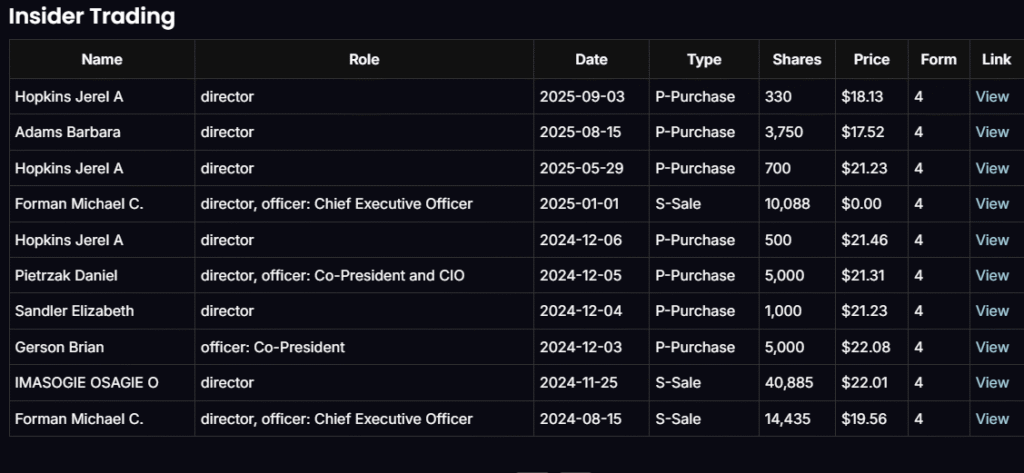

🕵️ Insider & Political Trades

- Recent insider purchases: Multiple directors (Hopkins, Adams, Pietrzak, Sandler, Gerson) bought shares between $17–22 in 2024–2025.

- Recent sales: CEO Michael Forman sold at $19–22 in 2024.

- Bullish Tilt: Small insider buys near current levels (~$17–18) suggest confidence, though the amounts are not huge.

Senate/House trades are older (2019–2021) and less relevant to today’s picture.

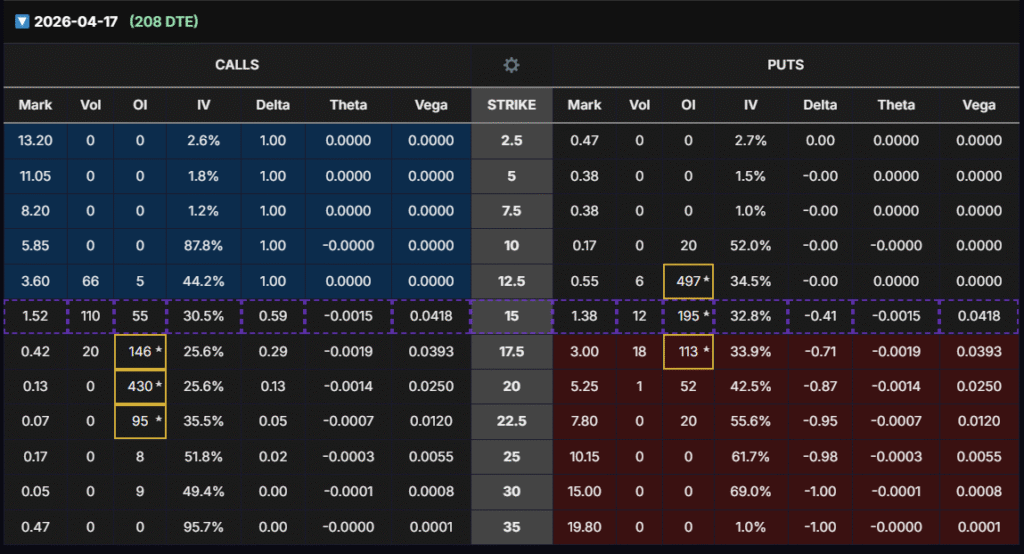

📈 Options Chain & LEAPS Strategy

- Chosen Contract: $15 Strike Call (Apr 17, 2026, 208 DTE).

- Delta: 0.59 → efficient directional exposure (option moves ~59% of stock’s move).

- Vega: 0.0418 → strong exposure to IV increases, which tend to spike into earnings.

- Open Interest: 195 (plus 110 new contracts traded today, likely rolling into OI).

- IV: ~30.5% → relatively cheap for a beaten-down stock.

🎯 Trade Thesis

We are targeting the $15 strike Apr 2026 Call because:

- It is at-the-money, giving the strongest mix of delta and vega.

- It has the highest liquidity near the money.

- Implied volatility is cheap to buy, setting us up to profit when IV expands before earnings.

This trade is not dependent on the stock breaking out significantly. Even a modest 10% stock rise can produce 30–40%+ gains in the option due to delta + vega amplification. A 20% rally combined with IV expansion could result in 2–3x returns.

📌 3-Batch Entry Strategy (Risk Management)

We will enter this trade in three batches to control risk and reduce timing pressure:

- Batch 1 (Now): Enter initial position at ~$1.52 option price.

- Batch 2 (1–2 weeks later): Enter again only if the option price drops –40% to –50%. (⚠️ Important: this refers specifically to the options price, not the stock price).

- Batch 3 (1–2 weeks after Batch 2): Enter final tranche if the Batch 2 options price also drops –40% to –50%.

By layering entries this way, we reduce cost basis and maximize payoff when volatility expands ahead of earnings.

⚠️ Disclaimer & Allocation Guidance

- This analysis is for educational purposes only and should not be considered financial advice.

- Allocate no more than 2% of your total portfolio to this strategy.

- Options involve substantial risk and may not be suitable for all investors.

- Always do your own research and consult a licensed financial advisor before making investment decisions.

✅ Bottom Line:

FSK is deeply oversold and trading near multi-year lows. The $15 Apr 2026 calls provide an attractive opportunity to benefit from both a modest price recovery and implied volatility expansion. By entering in three controlled batches and keeping allocation small, we set up a favorable risk/reward play in an otherwise high-risk, high-yield stock.