Centene Corporation (CNC) has been on a volatile ride in 2025, recently hitting a five-year low in August before beginning a tentative rebound. At the current price of $28.98, CNC sits well below historical highs, but technical indicators are hinting that a recovery phase may be underway. For long-term traders and option strategists, this environment presents a compelling opportunity to capture value through both price recovery and implied volatility expansion.

🔹 Technical Analysis

On the 5 year chart, CNC shows a clear breakdown pattern from its multi-year highs, with the stock collapsing sharply into the low $20s in August. That drop brought the RSI deep into oversold territory, but in recent weeks, RSI has been climbing back, now sitting just above 25.62. This move signals a potential shift away from extreme bearishness.

The MACD also supports a rebound thesis. After months of downward pressure, CNC registered a bullish crossover between July and August, with histogram bars now reflecting momentum returning to the upside. The stock has yet to regain a strong uptrend, but the combination of stabilizing price action, rising RSI, and MACD crossover suggests accumulation at these depressed levels.

Zooming into the 1 year chart, CNC is steadily climbing back from its oversold base. RSI has normalized to around 47.8, suggesting the stock is no longer oversold. The MACD line is above the signal line, further confirming momentum in favor of bulls. This technical setup aligns with the idea that CNC may be carving out a short-term bottom before staging a larger recovery.

🔹 Financial Overview

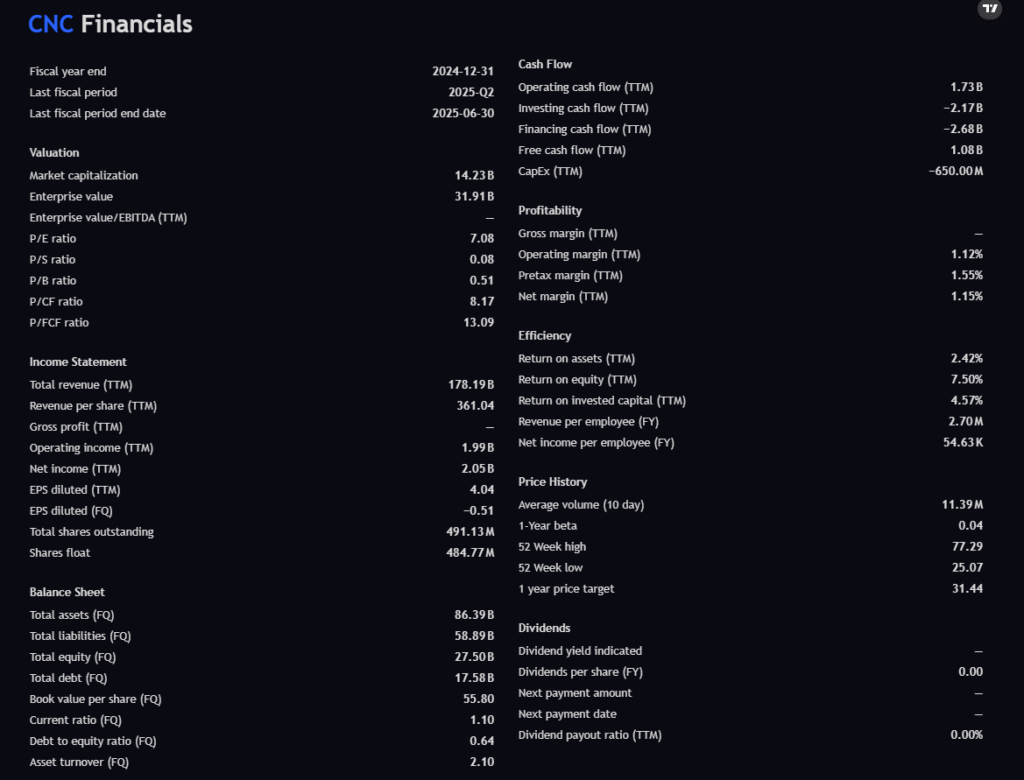

Despite its sharp price drop, CNC maintains solid financial footing. Free cash flow sits at $1.08B, a healthy cushion that allows the company flexibility. While net margin (1.15%) and operating margin (1.12%) are slim, they remain positive, which is crucial given the current pressure on healthcare providers.

CNC trades at a P/E ratio of 7.08, well below the broader market average, signaling potential undervaluation. The debt-to-equity ratio of 0.64 indicates moderate leverage, not alarming but worth watching given the low margins. With total assets of $86.39B and total equity of $27.50B, CNC still stands as a large and stable player in the managed healthcare sector.

The biggest weakness is profitability — thin margins leave CNC vulnerable to reimbursement changes and cost overruns. However, its cash flow strength and valuation discounts provide a margin of safety for investors betting on stabilization.

🔹 Analyst Sentiment

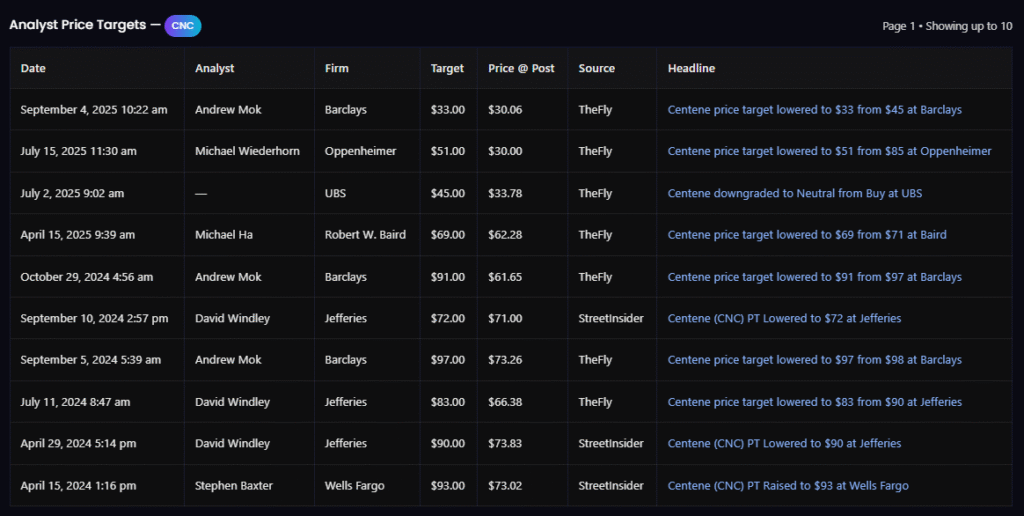

Analysts have sharply revised CNC’s targets downward over the past year. Barclays recently cut its target to $33 (from $45), while Oppenheimer reduced its view to $51 (from $85). UBS set a neutral rating with a $45 target.

Despite the downgrades, every recent target still sits above the current price of $28.98. The median of recent targets ($43) implies roughly +48% upside from today’s levels. While sentiment has shifted from bullish to neutral, analysts agree that CNC remains undervalued relative to its fundamentals.

🔹 Options Strategy: LEAPS Trade Setup

For investors looking to capitalize not only on price recovery but also on implied volatility dynamics, a LEAPS (Long-Term Equity Anticipation Securities) strategy offers attractive risk/reward.

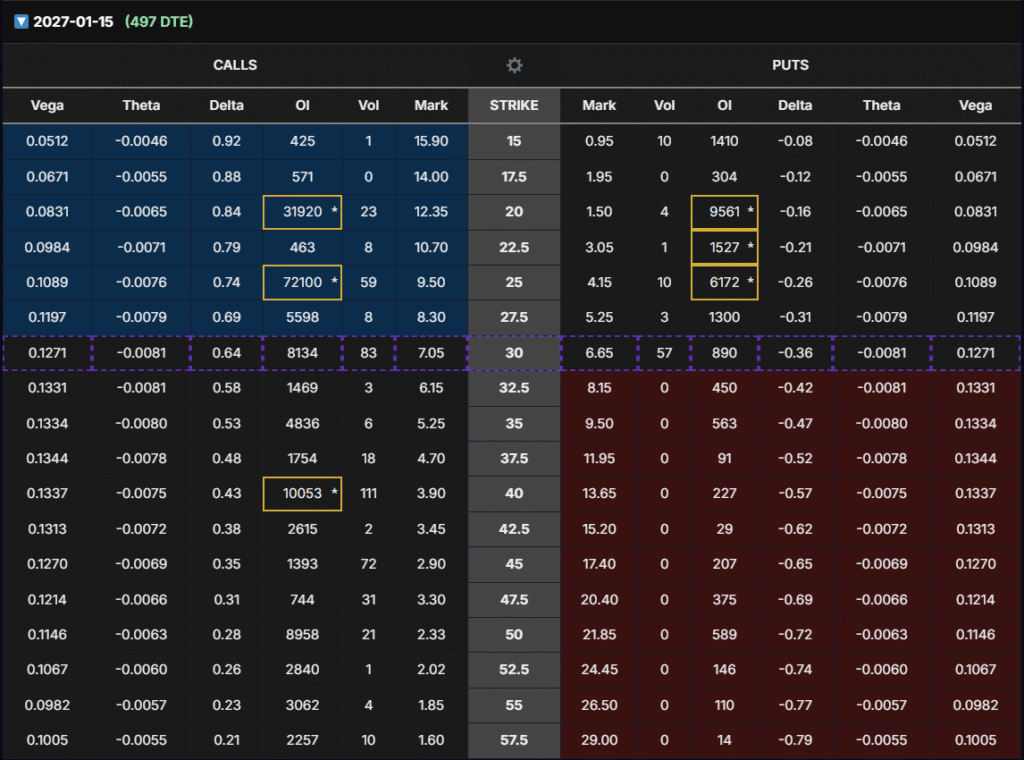

- Trade Selection: Buy CNC Jan 2027 $40 Call @ ~$3.90 (Mark Price).

- Delta: ~0.43 → Provides balanced exposure to price moves.

- Vega: ~0.1337 → Every 1% increase in implied volatility boosts the option by ~$0.13.

- OI: 10,000+ contracts → Strong liquidity.

- Theta: Minimal at -0.0075 per day → Very little time decay.

🔹 Profitability Scenarios

- IV Expansion Only: If implied volatility rises +10% before earnings, the option could gain ≈ $1.33 per contract (+34%).

- Stock Price Rise Only: If CNC rises $5 to ~$34, the option gains ≈ $2.15 per contract (+55%).

- Both Together: Stock rally +$5 AND IV expansion +10% → Option could gain ≈ $3.50–3.70, nearly doubling (+90%).

This setup allows traders to leverage both Delta and Vega, selling into IV expansion before earnings rather than waiting for expiration. The limited cost ($390 per contract) also provides defined risk.

🔹 Conclusion

CNC sits at a critical juncture. The charts show early signs of recovery after a capitulation low, financials highlight a company with strong cash flow but thin margins, and analyst targets suggest meaningful upside despite recent downgrades.

For stock investors, CNC offers deep value at current prices. For options traders, the Jan 2027 $40 LEAPS call provides a strategic way to ride both price recovery and volatility expansion into catalysts.

With careful timing — exiting ahead of earnings when Vega inflates — this trade could deliver outsized returns compared to the stock alone.