Date: September 3, 2025

Time Horizon: 12–24 Months

Strategy Focus: LEAPS (Long-Term Equity Anticipation Securities)

🧱 Technical Analysis

Looking at CNH Industrial from a technical perspective, the stock is trading at $11.21, which places it very close to its 1-year lows and also near a long-term support zone that has held multiple times over the past five years. This is a critical level because the stock has historically shown strong rebounds when testing this price area.

On the 1-year daily chart, the Relative Strength Index (RSI) is currently at 28.65, which is firmly in oversold territory. While oversold readings don’t guarantee immediate reversals, they are often early indicators that downside pressure is exhausting itself. The MACD indicator is still in bearish crossover mode, suggesting that near-term momentum remains negative, but once the histogram flattens, it could set up a bullish reversal.

The 5-year weekly chart reinforces this view. Support around $10–11 has acted as a floor multiple times in the past, and we are once again testing this zone. The weekly RSI is at 39.65, which is not yet deeply oversold, but does confirm weakening momentum. Taken together, these signals suggest that while the stock may have a little more downside left, the reward/risk ratio improves significantly once the technical reversal is confirmed.

💵 Fundamental Analysis

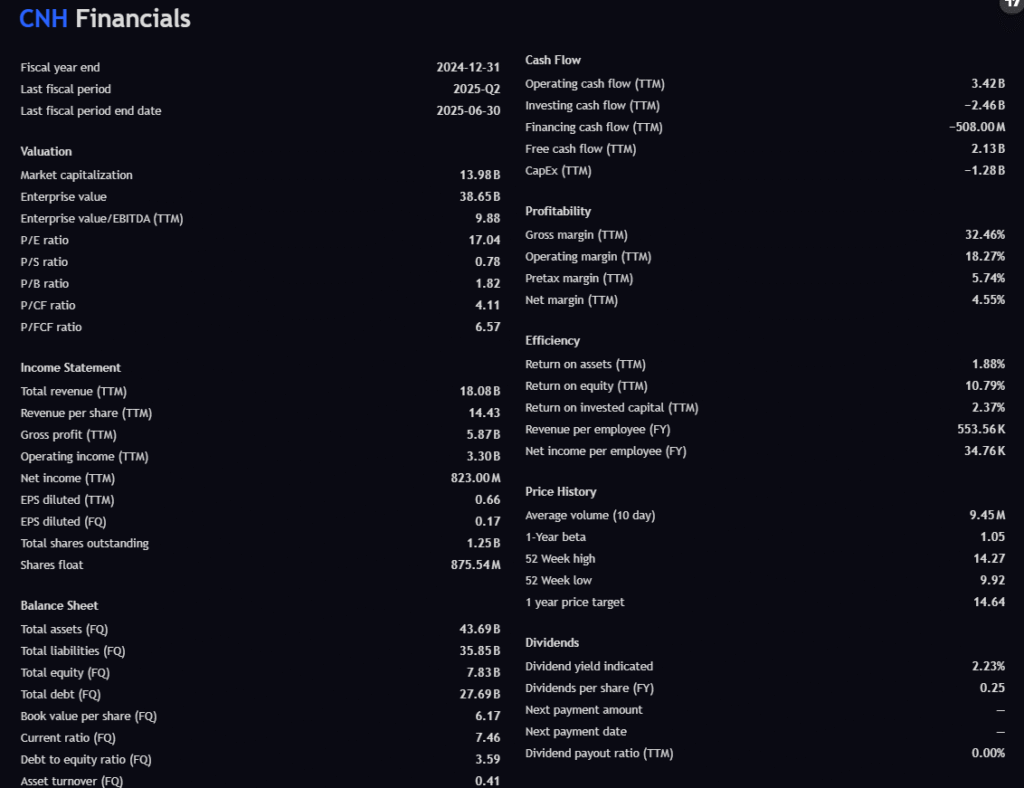

Fundamentally, CNH Industrial is a cash-generating business with a strong revenue base and relatively cheap valuation. The company generated $18.0 billion in trailing twelve-month revenue, with gross profit of $5.87 billion and operating income of $3.30 billion. Net income, however, was slimmer at $823 million, reflecting the capital-intensive nature of the industrial sector.

What really stands out is the free cash flow (FCF) profile. With $2.13 billion in positive FCF, CNH demonstrates the ability to cover debt obligations, reinvest in the business, and potentially return value to shareholders. The P/FCF ratio of just 6.57 makes this stock attractive on a cash flow valuation basis. For long-term options investors, strong cash flow reduces the risk of dilution or solvency issues over the lifespan of LEAPS contracts.

Valuation multiples are also supportive. The P/E ratio of 17.04 is reasonable, especially compared to industrial peers. The P/S ratio of 0.78 signals that the market is undervaluing CNH on a sales basis, since anything under 1 is often considered cheap. The P/B ratio of 1.82 shows the company is trading only modestly above its book value.

The main weakness is the balance sheet. CNH carries $27.7 billion in debt, with a debt-to-equity ratio of 3.59. While this leverage is high, the company’s current ratio of 7.46 suggests liquidity is more than sufficient to manage short-term obligations. This means debt is a long-term challenge but not an immediate risk.

📈 Analyst Price Targets

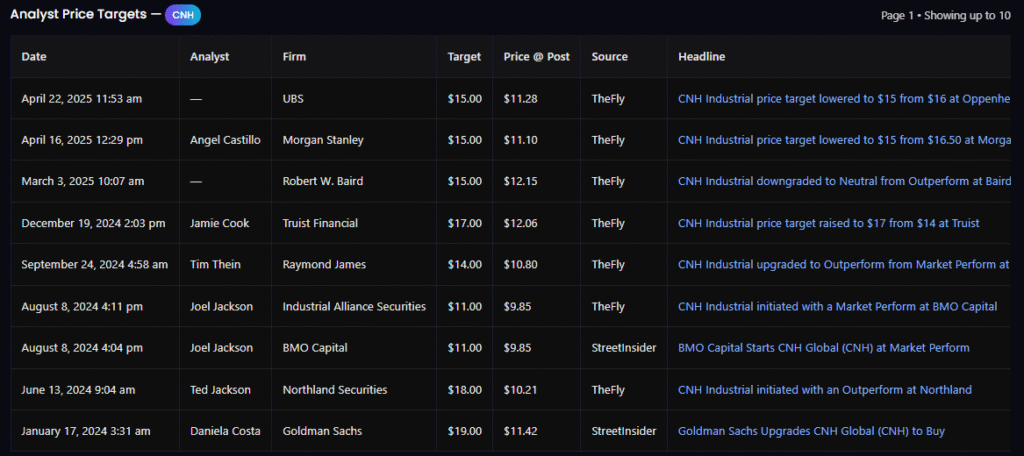

Analyst coverage is consistent in projecting upside. Over the past year, major firms including UBS, Morgan Stanley, Baird, Truist, and Goldman Sachs have set price targets ranging from $14 to $19. The consensus cluster is around $14–15, which implies about 30% upside from current levels. The high-end bullish targets of $18–19 suggest a potential 60–70% gain if macro conditions support industrial growth.

Even with some downgrades in 2025, such as UBS trimming its target from $16 to $15, analysts are still maintaining expectations above the current price. Importantly, the bullish upgrades from firms like Truist and Goldman Sachs indicate confidence in CNH’s long-term fundamentals.

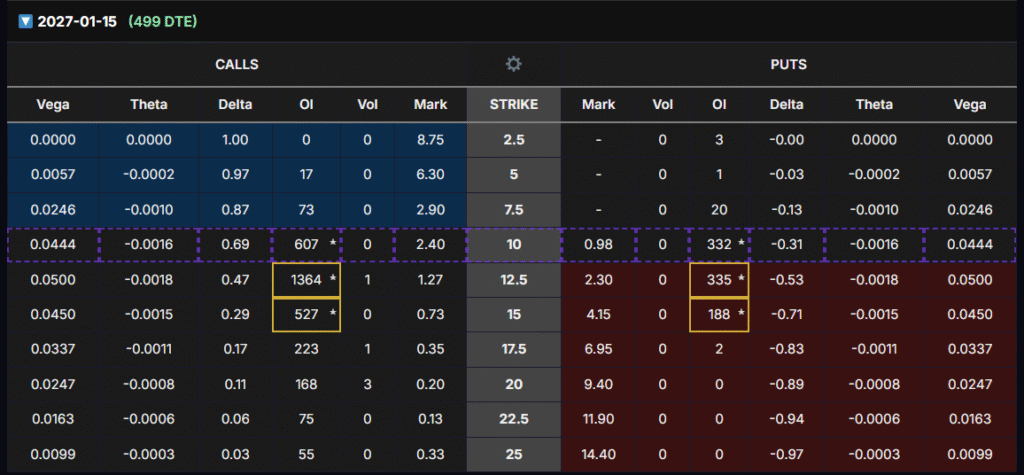

📝 Options Chain Analysis (Jan 15, 2027, 499 DTE)

Looking at the January 2027 option chain, which has nearly 500 days until expiration, three strikes stand out:

- $10 Strike (ITM): Delta 0.69, Vega 0.0444, Premium $2.40. This is the safer, stock-like play. Gains will closely mimic stock appreciation, but vega sensitivity is lower.

- $12.50 Strike (ATM): Delta 0.47, Vega 0.0500, Premium $1.27. This is the sweet spot for LEAPS investors. It has the highest vega, strong liquidity (OI 1,364), and balanced delta exposure.

- $15 Strike (OTM): Delta 0.29, Vega 0.0450, Premium $0.73. This is the speculative choice. If CNH rallies toward analyst targets ($16–19), this contract provides the highest percentage return, but also the greatest risk of expiring worthless.

For a strategy that prioritizes vega gains (sensitivity to implied volatility), the $12.50 strike is the most compelling choice. It balances cost, delta exposure, and volatility sensitivity in a way that maximizes upside while controlling risk.

🧩 Final Thesis

CNH Industrial offers a compelling mix of technical oversold conditions, undervalued fundamentals, supportive analyst targets, and attractive LEAPS pricing. The stock is currently not ready for entry, as momentum remains bearish, but once technical confirmation arrives, it has the potential to deliver significant long-term gains.

For LEAPS investors, CNH is a textbook candidate:

- Primary Candidate: Jan 2027 $12.50 Calls (best vega/delta balance).

- Conservative Choice: Jan 2027 $10 Calls (lower risk, higher delta).

- Aggressive Play: Jan 2027 $15 Calls (cheap, high upside, high risk).

📌 Conclusion: Put CNH on Your Watchlist

With oversold technicals, strong cash flow, and analysts projecting 30–60% upside, CNH Industrial should be monitored closely for a reversal signal. Once that occurs, this name becomes one of the more attractive long-term options setups in the industrial sector.

[PLACEHOLDER: Payoff Scenarios Chart if added]

⚠️ Disclaimer: This analysis is for informational purposes only. No position is currently held in CNHI. Options involve significant risk and may not be suitable for all investors.